Construction Economics and Building

Vol. 26, No. 2

2026

ARTICLES (PEER REVIEWED)

Assessing Risk Analysis and Management Practices of Property Development Companies in Nigeria

Obinna Collins Nnamani*, Joseph Ugochukwu Ogbuefi

Department of Estate Management, Faculty of Environmental Studies, University of Nigeria, Enugu Campus, Enugu, Nigeria

Corresponding author: Obinna Collins Nnamani, collins.nnamani@unn.edu.ng

DOI: https://doi.org/10.5130/zrjpg380

Article History: Received 01/03/2025; Revised 24/06/2025; Accepted 22/07/2025; Published 19/06/2026

Citation: Nnamani, O. C., Ogbuefi, J. U. 2026. Assessing Risk Analysis and Management Practices of Property Development Companies in Nigeria. Construction Economics and Building, 26:2, 1–22. https://doi.org/10.5130/zrjpg380

Abstract

Risk is inherent in property development, yet its management remains a challenge in many emerging economies. This study is aimed at assessing the risk management practices of real estate development companies in Nigeria, providing a comprehensive understanding of how risks are analysed and managed across the country’s six geopolitical zones. This study employed an explanatory sequential mixed-methods design to investigate the risk management practices of real estate development companies in the six geopolitical zones of Nigeria. While 250 questionnaires were sent to development firms registered with the Real Estate Developers Association of Nigeria, personal interviews were conducted with 13 purposively selected developers. Quantitative data were analysed using descriptive statistics, while qualitative data were analysed using a thematic approach. Out of the 250 questionnaires distributed, 84 were correctly filled out and returned, giving a response rate of 33.6%. Descriptive statistics results showed that out of 31 risk management techniques, brainstorming, checklists, experience/judgement/intuition, risk avoidance, and interviews were the most commonly used techniques adopted by real estate developers in risk management for development projects. Additionally, over half of the development firms have well-formulated strategies for risk management; however, this does not translate into practice. The qualitative findings validated most of the quantitative results. This study inferred that combining qualitative with quantitative methods, especially probabilistic approaches, will create a comprehensive and more balanced risk management approach in real estate development projects. The findings of this study would assist both local and international developers in making informed decisions regarding real estate development investment in Nigeria and other countries that share similar characteristics with Nigeria.

Keywords

Risk Management; Risk Analysis; Real Estate Development; Mixed-Methods; Nigeria

Introduction

Project risk management plays a fundamental role in mitigating risk and uncertainty in project execution. Although there is substantial evidence that risk management tools, encompassing processes and models, both qualitative and quantitative, have been developed for project appraisal, the current debate/argument is on practical application and the competency required to apply them (Zhang et al., 2014; Zou et al., 2017). Real estate development, despite being one of the most speculative ventures (Byrne, 2002), continues to lag behind other industries in adopting advanced techniques for risk identification, evaluation, mitigation, and control. As Reed and Sims (2015, p. 107) observed, “Developers are often criticised for not sufficiently understanding and analysing the level of risk.” In contrast, sectors such as finance, insurance, and banking have long embraced sophisticated risk management tools and methodologies, supported by an extensive body of research. However, studies on risk management practices within the property development industry remain limited (Whipple, 1988; Moorhead et al., 2021), especially so in emerging market economies like Nigeria.

In Nigeria, numerous instances of property development failures and abandonment have led to significant social, environmental, and economic challenges. Numerous development projects are left incomplete, while others, even after completion, remain unsold or unoccupied for over 6 months. In some cases, lenders foreclose on completed projects due to developers’ inability to repay loans, resulting in widespread financial distress and losses. For example, hundreds of abandoned housing projects can be found across the country. A financial expert from the Federal Mortgage Bank of Nigeria reported that loan defaults by developers and mortgage bankers have amounted to over ₦100 billion, which the bank has been unable to recover (Adegboye, 2018).

Some specific issues affecting the property development sector in Nigeria include the following:

• Non-performing loans in real estate and construction from selected banking sector data totalled ₦226.62 billion as of 2020, based on selected data from the banking sector (NBS, 2021).

• A significant portion of newly built accommodation each year remains abandoned, vacant, or incomplete as a result of ineffective demand (Centre for Affordable Housing Finance in Africa, CAHF, 2020).

• Between 1974 and July 2021, Nigeria recorded a total of 461 building collapses, resulting in over 1,090 deaths and numerous injuries. Lagos state accounted for the highest number, with 295 cases (Ghonegun & Olorunlomeru, 2021).

• The financial ruination of development firms, the impact of loan default on development lenders, and the overall low stock of real estate in Nigeria (Ogbuefi, 2002; Saidu & Yeom, 2020).

The significance of studying risk management in property development projects in Nigeria cannot be overstated, considering the substantial socio-political and economic challenges. It is evident that the current volatile and uncertain development environment significantly hinders effective decision-making in real estate development initiatives.

Real estate development is a highly complex and risky endeavour, with significant social, economic, and environmental consequences in the event that projects fail. Although the development process is very crucial to the economic growth and development of a nation, there is limited substantive research that has been conducted relating directly to real estate development. While research on risk and general risk management is well documented, there are few empirical studies on how development companies/organisations manage risks. Documented literature has extensively investigated the risk analysis and management within the context of investment in existing income-generating property, yet there is limited empirical studies in the development sector, notwithstanding that real estate development poses a different set of risks—construction cost overruns, construction delays, changes in interest rate, absorption rate, initial lease-up rents, rent concessions, etc. (Ratcliffe et al., 2021).

Despite the modest advancement made by extant studies (Wiegelmann, 2012; Ayodele & Olaleye, 2021; Moorhead et al., 2021), there are research gaps that this study has identified and attempted to fill. For instance, none of the above and other previous studies (Fisher & Robson, 2006; Preller, 2009; Gehner, 2008) seem to have investigated risk management practice across the different stages of the risk management process.

This study, which forms part of a broader study on risk management practices in Nigeria, assessed the risk analysis and management practices of real estate development companies in the country. The paper is structured into six sections. The first section highlights the study’s context, aim, and relevance. The second section presents a literature review on the application of risk management techniques in real estate development, including the identified knowledge gap. The third section outlines the research methodology in a manner that allows for replication. The fourth section presents the study results in tabular form and charts, accompanied by concise analyses. The fifth section discusses the results, their significance, and their relation to previous studies. The final section summarises the key findings and their practical implications. This is the first study to comprehensively assess the risk analysis and management practices of real estate developers across Nigeria’s six geopolitical zones. The findings will assist both local and international developers in making informed decisions on risk analysis and management practices. Furthermore, the study contributes to the literature on real estate development risk from an emerging market perspective.

Literature review

Concept of risk management

The concept of risk management has been described in various ways throughout the literature. According to Berg (2010, p. 81), a widely accepted definition of risk management is that “risk management is a systematic approach for determining the optimal course of action under uncertainty by identifying, evaluating, understanding, acting on, and communicating risk issues.” Particularly relevant to this study is the definition by Wiegelmann (2012, p. 61), citing Deloach (2000): “Risk management is a structured and disciplined approach that aligns strategy, processes, people, technology, and knowledge with the purpose of evaluating and managing the uncertainties a real estate development organisation faces as it creates value.” Central to this definition is the idea that risk management involves a systematic process encompassing all organisational regulations and procedures for identifying, analysing, assessing, and controlling all potential risks, as well as managing the profitability and efficiency of any actions taken.

Risk management frameworks and standards differ in their composition of stages or steps within the risk management process models. The Committee of Sponsoring Organizations of the Treadway Commission Enterprise Risk Management (COSO ERM) model comprises eight interconnected components: internal environment, objective setting, event identification, risk assessment, risk response, control activities, information and communication, and monitoring. From the project management perspective, the Project Management Body of Knowledge (PMBOK) (2017) project risk management outline includes the following steps: risk management planning, risk identification, qualitative risk analysis, quantitative risk analysis, risk response planning, risk response implementation, and risk monitoring. Taking into consideration the various risk management techniques applied at different stages of the process, there is a general consensus in the literature that the process consists of four core steps (Makui et al., 2010). These steps are as follows: risk identification and classification, risk analysis, risk response, and risk monitoring.

Table 1 presents stages in the risk management process of the different organisations. While PMBOK (2017) and Alschuler and Dawson (2004) contain numerous stages, the Association for Project Management (APM) (2012) is more concise (Table 1). Notwithstanding this disparity, the essential structure of all these frameworks is analogous and can be reduced to three fundamental stages based on the Project Management Institute and APM frameworks (Kutsch & Hall, 2010). For this study, these stages include risk identification/classification, risk analysis, and risk response as illustrated in Table 2.

| Organisation | Stages in risk management process |

|---|---|

| PMI (2017) | • Plan risk management |

| • Identify risks | |

| • Perform qualitative risk analysis | |

| • Perform quantitative risk analysis | |

| • Plan risk response | |

| • Implement risk response | |

| • Monitor risks | |

| APM (2012) | • Initiate |

| • Identify | |

| • Assess | |

| • Plan responses | |

| • Implement responses | |

| Alschuler and Dawson (2004) | • Internal environment |

| • Objective setting | |

| • Event identification | |

| • Risk assessment | |

| • Risk response | |

| • Control activity | |

| • Information and communication | |

| • Monitoring |

Sources: PMBOK (2017), APM (2012), and Alschuler and Dawson (2004).

PMI, Project Management Institute; APM, Association for Project Management; COSO, Committee of Sponsoring Organizations; PMBOK, Project Management Body of Knowledge.

Risk identification and classification is a critical step in the risk management process, as it aims to establish the sources and nature of risks (Banaitiene et al., 2011). The first task is to identify all the risk factors associated with real estate development projects. These risk factors are identified using expert judgement and data-gathering techniques such as checklist analysis, interviews, and brainstorming, as well as strengths, weaknesses, opportunities, and threats (SWOT) analysis, stakeholder analysis, and cause-and-effect diagram (Gehner, 2008; PMBOK, 2017). The output of this process is a risk register, which lists the overall risk factors that could potentially affect the project outcome (PMBOK, 2017). This register serves as a key input for the risk analysis phase. In this context, risk analysis refers to the computation and synthesis of specific risk occurrences and uncertainties in order to appreciate their individual impact and/or their combined effects on project objectives (APM, 2019). Risk response follows the identification, analysis, and prioritisation of risks. At this stage, various options are developed and strategies are selected to address both individual and overall project risk exposures (PMBOK, 2017). Risk response strategies include avoidance, transfer, mitigation, and acceptance.

The quality of risk management is enhanced when it is implemented within a comprehensive framework. A total of 31 techniques were identified through a review of the literature (Table 2). Of these, 11 techniques fall under the risk identification and classification stage, 16 under risk analysis, and four under risk response.

Risk analysis and management practices in real estate development projects

Before the turn of the millennium, very few studies, such as the one reported by Whipple (1988), had investigated the risk management practices of real estate development companies during the development process. Prior to and immediately after the millennium, most studies have focused on the construction industry (see, for example, Akintoye & MacLeod, 1997; Uher & Toakley, 1999; Baker et al., 1999; Raz & Michael, 2001; Lyons & Skitmore, 2004), of which property is a sub-sector. These studies have examined various stakeholders within the construction industry, including property developers. Following this trend, a reasonable number of studies have begun to explore risk management in property development projects, particularly in developed economies such as the UK, the United States, Australia, and the Netherlands. Nevertheless, Crosby et al. (2020) observed that, despite the financial risks and inherent uncertainty associated with real estate development projects, fewer investigations had been conducted on real estate development compared to real estate investment in terms of performance and appraisal.

Akintoye and MacLeod (1997), considering other objectives, conducted a study on the use of risk management techniques using a sample of 100 top firms in the UK construction industry, comprising 30 project management practices engaged in building construction and 70 general contractors. The study achieved a 43% response rate, consisting of 30 general contractors and 13 project management practitioners. Their findings showed that approximately77% of contractors and 100% of project management firms used intuition/judgement/experience in risk analysis, followed by sensitivity analysis, applied by approximately53% of contractors and 38% of project management practitioners. Only approximately3% of contractors applied the Monte Carlo simulation. Uher and Toakley (1999) surveyed 713 Australian construction firms, receiving responses from 200 companies, of which 37 were property developers. Their study examined the skill levels and attitudes of key actors toward risk management during the conceptual phase of the construction project development. Subjective judgement emerged as the most commonly employed risk analysis technique, followed by sensitivity analysis. Knowledge of probability analysis, risk-adjusted discount rates, and decision tree methods was found to be inadequate. The most frequently used risk identification techniques were brainstorming, checklists, and flowcharts.

Baker et al. (1999) examined the risk management practices of 40 construction companies and 12 oil and gas firms in the UK, revealing that these companies use both qualitative and quantitative techniques. Qualitative approaches included brainstorming, interviews, expert experience, fuzzy set analysis, and historical contingency, with no remarkable differences in use across industries. Quantitative techniques varied: while construction firms used scenario analysis, break-even analysis, and monetary value method, oil companies employed more advanced tools such as algorithms, decision matrices, expected net present value, decision trees, and simulations. Both sectors favoured risk reduction strategies. Similarly, Lyons and Skitmore (2004), in a survey of 44 Queensland engineering construction firms, found that risk identification and risk analysis were prioritised over risk response and documentation. Common risk identification techniques included brainstorming, case-based approach, and checklists. Risk analysis relied primarily on intuition, experience, and judgement, followed by sensitivity analysis and risk premiums. The use of the Monte Carlo simulation, decision analysis techniques, and expected monetary value (EMV) was limited. Risk reduction emerged as the most widely applied risk response strategy.

In summary, findings from the above studies (1997–2004) showed that the most widely used risk analysis technique in the construction industry was intuition/judgement/experience. Empirical evidence also suggested that the oil and gas industry was more advanced than the construction industry in applying sophisticated risk analysis techniques. These studies were conducted in the UK and Australia and focused broadly on the construction industry, with none specifically examining the application of risk management techniques by property development companies. Between 2006 and 2012, more studies specifically focused on developers were conducted (e.g., Gehner et al., 2006; Gehner, 2008; Wiegelmann, 2012).

Gehner et al. (2006) surveyed 31 of the largest real estate developers in the Netherlands, including independent development companies, financier-related, contractor-related, investor-related, and other categories (e.g., owner-users and housing corporations). A total of 15 developers responded: seven independent developers, three financier-related, three contractor-related, one investor-related, and one in the remaining categories. For risk analysis, their results showed that all developers (100%) used intuition/experience and qualitative description, while 80% used scenario/sensitivity analysis. Risk premium was applied by 27%, checklists by 20%, total risk exposure assessment by 13%, and probabilistic techniques by 0%. These findings indicate that intuition/experience and qualitative description were the most commonly used techniques, followed by scenario/sensitivity analysis. No developer employed probabilistic techniques. This study was unique in focusing solely on property developers, unlike the previous studies. However, it did not explore the organisational structure of the decision-making process within the firms. Gehner (2008), in Knowingly Taking Risk: Investment Decision Making in Real Estate Development, described how development decisions were made within property development organisations. Only three firms were examined due to the descriptive and in-depth nature of the study. The findings revealed a low use of explicit risk analysis techniques in the investment decision-making process. Boardroom decision-making typically involved implicit scenario analysis through “what-if” questions, which were rarely quantified unless under extreme circumstances. The focus on only three Dutch case studies limits the generalisability and broader insights of the study.

Wiegelmann (2012) investigated the application of risk management techniques in leading European property development organisations. The study focused on organisational decision-making, using the COSO Risk Management Framework by Alschuler and Dawson(2004) due to its widespread acceptance within the European context. Addressing the limitations identified in Gehner’s (2008) study, Wiegelmann surveyed 69 major property development companies in the UK, Germany, Italy, France, Switzerland, Spain, and Austria, achieving a 43.7% response rate. His results revealed that approximately 69.9% of the firms approached risk assessment subjectively and intuitively. Established methods such as sensitivity analysis and scenario techniques were each used by 45%of respondents. Probabilistic techniques were the least used: the Monte Carlo simulation (10.1%), value at risk (7.2%), and decision tree analysis (4.3%).

From the Nigerian perspective, several studies have explored risk management practices in the real estate sector (e.g., Ogunba, 2002; Otegbulu et al., 2011; Nnamani, 2017). Ogunba (2002) investigated the use of risk analysis techniques by development surveyors, corporate developers, and development lenders during pre-development appraisals in Southwestern Nigeria. The study surveyed 193 surveying firms, 111 development lenders, and 18 corporate developers, with actual responses from 113 surveyors, 32 lenders, and 10 corporate developers. Their findings showed that none of the groups employed probabilistic risk analysis techniques in their pre-development appraisals. Otegbulu et al. (2011) examined risk assessment techniques used in property development projects in Abuja, Nigeria, assessing80 estate surveying and valuation firms. A total of 69 responded, including 23 project managers, 20 developers, 14 feasibility consultants, and 12 firms performing all three functions. The study found that the most frequently used risk analysis techniques were qualitative description and scenario/sensitivity analysis. Nnamani (2017) revealed that subjective assessment (88%) was the most commonly used technique during risk analysis among estate surveyors and valuers, followed by sensitivity analysis (60%) and risk-adjusted discount rate (36%).

This literature synthesis reveals that intuition, judgement, experience, and qualitative description remain the most commonly used risk management techniques adopted by developers. While there has been a slight improvement in the use of sophisticated risk management techniques like the Monte Carlo simulation, subjective assessment remains the most commonly used technique (Moorhead et al., 2021). Importantly, it should be noted that neither the Nigerian studies nor those from more advanced markets used the full risk management process framework to examine the adoption of risk management techniques by developers during the development process.

Research method

This study employed an explanatory sequential mixed-methods research design (Cameron, 2009). This form of mixed-methods design combines quantitative and qualitative methods aimed at investigating the adoption of risk management techniques by real estate development companies in the six geopolitical zones of Nigeria: North–Central, North–East, North–West, South–East, South–South, and South–West. The justification for adopting the mixed-methods model is that integrating quantitative and qualitative data provides deeper insight beyond the information either could offer independently. Neither quantitative nor qualitative approaches alone could adequately provide a thorough understanding of the risk management practices of the real estate development firms within the area of investigation. The mixed-methods model comprises a two-stage data collection process. Firstly, quantitative data were collected through surveys and analysed, followed by a personal interview as recommended by Creswell and Creswell (2018). Figure 1 shows the explanatory sequential mixed-methods design protocol.

Figure 1. Explanatory sequential design (two-phase design). Adapted from Creswell and Creswell (2018)

The study population comprised 1,906 property development companies registered with the Real Estate Developers Association of Nigeria (REDAN) as of March 4, 2021. For the survey, an adjusted sample size of 245 companies was determined using the Krejcie and Morgan (1970) formula, and this was proportionally allocated across the six geopolitical zones using Okafor’s (2002) formula (see Table 3). For the personal interviews, a total of 13 public and private firms were purposively selected. Two firms were selected from each state, except Lagos, which was allocated three firms. The selection was based on the demographic characteristics of the firms, their responses to the survey questionnaire, and other key indicators such as firm size, ownership structure, developer type, and years of experience. Kvale and Brinkmann (2009) and Kvale (1996) recommended a sample size of between five and 25 for qualitative studies. Accordingly, the sample size of 13 interviewees was considered adequate.

| State | North-Central | North-East | South-East | North-West | South-West | South-South | Total |

|---|---|---|---|---|---|---|---|

| Sample size | 131 | 2 | 9 | 8 | 86 | 9 | 245 |

The primary data were collected in two distinct phases/stages. In the first phase, the quantitative data were collected using survey questionnaires that were administered to top management personnel in each of the sampled property development companies. The questionnaire[comprising the characteristics of the development companies and 31 risk management techniques adapted from existing literature (see Table 2)] and personal interview questions with developers were face-validated by five experts, including two senior academics in real estate, two industry professionals, and a statistician (Taherdoost, 2016). A pilot study was conducted by distributing 20 questionnaires to respondents selected from states within each of the six geopolitical zones. The aim was to test the reliability of the scale and the internal consistency of the variables using Cronbach’s alpha, a common measure of reliability. Cronbach’s alpha test yielded a reliability coefficient of 0.802, indicating a strong reliability for the study (Debrah et al., 2020). The survey questionnaire was distributed using online surveys and drop-and-collect approaches in order to achieve optimum response from the respondents. The drop-and-collect approach was adopted using field assistants who were trained and briefed on how to distribute and collect the survey instrument from the respondents. The questionnaire, designed using the Google Form, was sent to the emails of some of the respondent firms. The emails were sourced from the REDAN directory. The Google Forms questionnaire was also distributed and collected through REDAN’s WhatsApp platform. The online survey and the drop-and-collect approaches made it difficult to determine the exact number of questionnaires distributed (Debrah et al., 2022). Nonetheless, approximately 250 questionnaires were distributed to the development companies.

In the second phase, qualitative data were collected through personal interviews with the 13 selected firms. The interview questions were informed by the results from the quantitative data analysis conducted in the first phase. Respondents for the in-depth oral interviews were purposefully selected from those who had completed the survey. This phase was designed to build directly on the quantitative results. The qualitative data were gathered through one-on-one oral interviews, conducted both in person and via the ZOOM platform. Each interview session lasted between 45 minutes and 1 hour 15 minutes, with an average duration of approximately 1 hour. All sessions were audio-recorded with the consent of the interviewees. The recordings from the 13 interviews were transcribed into text using the Descript software. The resulting transcripts were thoroughly edited and carefully reviewed to ensure accuracy, with necessary corrections and adjustments made as appropriate.

The quantitative data were collected between July 2021 and January 2023. The quantitative data analysis spanned a period of 3 months (from February to April 2023), while the qualitative data collection took place from June 2023 to March 2024. Questionnaire instruments and personal interviews were considered the most appropriate instruments of data collection for this study because they complemented each other to generate detailed information and standardised responses vis-à-vis the explanatory sequential mixed-methods design. The quantitative data retrieved from the questionnaire survey were transferred to the MS Excel worksheet and analysed using Statistical Package for the Social Sciences (SPSS) version 26. The data were analysed using frequency and percentage. In contrast, NVivo 14 was used for the qualitative data analysis by adopting the thematic content analysis technique as recommended by Braun and Clarke (2006).

Frequency and percentage were used to analyse the data on development firms’ profiles and also the adoption of the 31 risk management techniques within the risk management process. Thematic content analysis was used to analyse the interview transcripts. The results are presented using texts, tables, pie charts, and bar charts.

Results and analysis

Presentation of quantitative results

Out of the 250 survey questionnaires distributed, a total of 84 completed questionnaires deemed suitable for evaluation were returned, resulting in an overall response rate of 33.6%. This response rate is relatively high, as Baruch and Holtom (2008) reported that organisational surveys typically record response rates ranging from 16.9% to 54.5%.

Figure 2 shows the distribution of the firms’ responses across the six geopolitical zones: North–Central zone 23 (27.4%), North–East zone 6 (7.1%), North–West zone 5 (6.0%), South–East zone 20 (23.8%), South–West zone 19 (22.6%), and South–South zone 11 (13.1%).

Figure 2. Distribution of firms within the six geopolitical zones in Nigeria.

The bar chart shows that the North–Central zone had the highest response rate, likely due to the concentration of large firms in the Federal Capital Territory (FCT). This was followed by the South–East and South–West zones. Lower response rates were recorded in the North–East and North–West zones. In the North–West, the low response rate may be attributed to the fact that many development firms operating in Kaduna are based in the FCT. Overall, both the North–East and North–West geopolitical zones had a relatively small number of real estate developers registered with the REDAN.

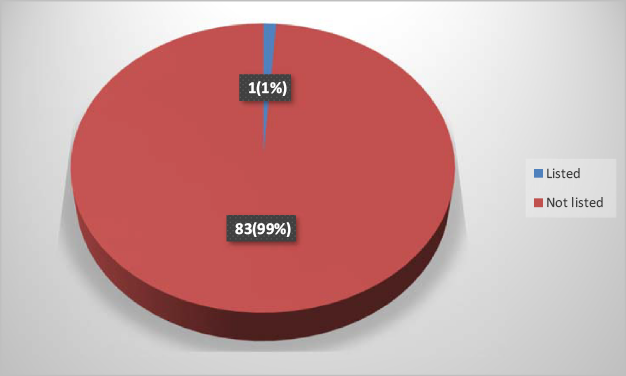

Figure 3 presents the proportion of companies listed on the Nigerian Exchange (NGX). Only 1% of the companies were listed, while 99% were not. These results suggest limited public accountability and transparency in risk management practices, as most real estate development companies operate privately without the regulatory oversight and disclosure requirements associated with NGX listing.

Figure 3. Proportion of companies listed on Nigerian Stock Exchange.

Table 4 shows that more than half of the companies (57.1%) had an average turnover of less than 400 million over the past 5 years. Based on the results, the companies were classified as small, medium, or large. In addition, annual turnover determines the level of resources available for risk management. Companies with higher turnover are most likely to allocate adequate resources for comprehensive risk identification, assessment, and control, while those with lower turnover may not (Wiegelmann, 2012).

Table 5 shows that more than half of the companies (53.6%) reported completing less than 50% of their development projects. Similarly, the majority of companies reported that abandoned, ongoing, and incomplete projects were below the 50% completion stage. These results suggest weak or inadequate risk management practices, as effective risk management is directly linked to higher project completion rates.

Table 6 presents the techniques adopted by developers for risk identification and classification. Brainstorming (71.4%) was the most widely used technique, followed by checklists (67.9%) and interviews (56.0%). The influence diagram was the least adopted. Overall, the results suggest that companies rely on basic rather than robust approaches for risk identification and classification.

Experience/judgement/intuition was the most commonly used risk analysis technique (64.3%), followed by sensitivity analysis (42.9%). The Monte Carlo simulation (2.4%) and algorithms (4.8%) were the least adopted. The results suggest a strong preference for intuitive and experiential methods among development companies (see Table 7).

The risk response techniques adopted are shown in Table 8. Risk avoidance was the most frequently used technique (63.1%), while risk transfer was the least used (15.5%). This implies that most firms do not insure their development projects.

| Technique | Frequency | Percentage |

|---|---|---|

| Avoidance | 53 | 63.1 |

| Transfer | 13 | 15.5 |

| Mitigation | 26 | 31.0 |

| Acceptance | 26 | 31.0 |

Overall, the most widely adopted risk management techniques included brainstorming (71.4%), checklists (67.9%), experience/judgement/intuition (64.3%), risk avoidance (63.1%), and interviews (56%). These results suggest that risk management in Nigeria’s real estate development sector is dominated by qualitative approaches, with limited adoption of advanced techniques. This reflects a maturing but still underdeveloped risk management culture, which has implications for the sector’s long-term sustainability and growth.

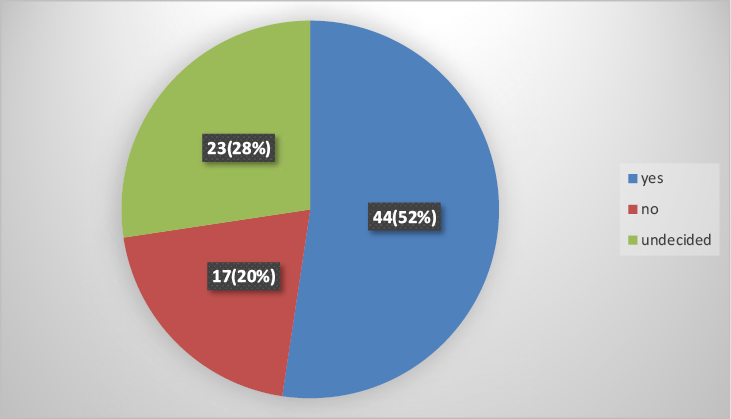

Figure 4 shows that 52% of the firms had a well-formulated strategy for managing risk, while 48% did not.

Figure 4. Firm’s formulation strategy for managing risk.

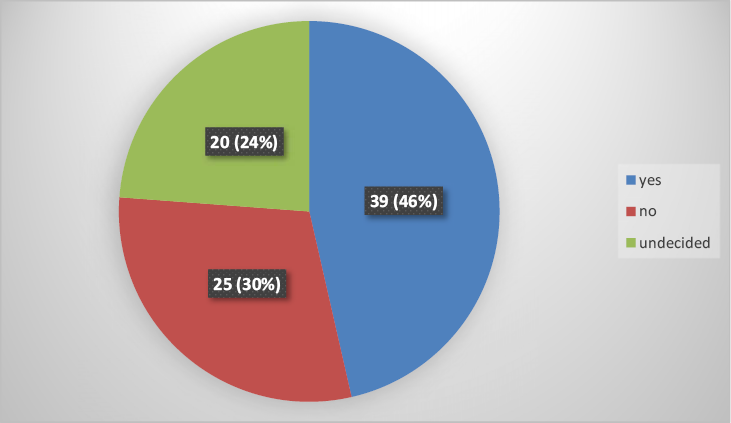

Figure 5 shows that 46% of the firms had a consistently defined risk catalogue used for risk identification, while 54% did not. These results suggest that the majority of companies lacked a standardised approach to cataloguing risks, which could result in poor decision-making, inconsistent risk responses, a higher likelihood of project delays or failures, increased exposure to unforeseen risks, and reduced investor and stakeholder confidence.

Figure 5. Firms’ consistent definition of risk catalogue for risk identification.

Table 9 shows that the chief executive officer was responsible for risk management in 36.9% of the companies studied. In 17.9% of companies, the operations officer handled risk management, while 23.8% reported having no designated staff responsible. Risk management experts and committees were responsible for 5.9% and 8.3% of the companies, respectively. This suggests that either the companies lacked the resources to hire risk management experts or they did not regard risk management as a critical function.

Presentation of personal interview findings and analysis

This section presents a summary of findings from the oral interviews regarding the risk analysis and management practices of development companies. The key themes examined include financial feasibility analysis (FFA); risk identification and classification, risk analysis, and response; adoption of risk management strategies; consistent use of a defined risk catalogue; and the staff primarily responsible for managing risks. While many of the qualitative findings align with the quantitative results, some remarkable differences also emerged.

FFA, also referred to as development appraisal, is a fundamental prerequisite for effective risk analysis (Havard, 2014). It is primarily used to assess the viability of a development project, helping determine the appropriate price to bid for land. Another major function of FFA is to evaluate whether a project is likely to generate a profit or incur a loss. By analysing data on projected costs and expected returns, FFA helps establish the overall feasibility of a development (Havard, 2014). Their findings from the oral interviews reveal that over 80% of the firms, both public and private developers, reported conducting FFA. Some public developers noted, however, that FFA is outsourced rather than performed internally. Additionally, only approximately 31% of the firms could specifically identify the tools they used for FFA, such as cash flow analysis and payback period calculations. Interestingly, an individual developer expressed doubt about FFA altogether, asserting that a good location alone guarantees investment success. This viewpoint suggests that many smaller, and possibly medium-sized, firms tend not to engage in large-scale or complex projects or in managing multiple developments simultaneously.

Under the application of risk management techniques, the firms’ respondents were asked about the risk management techniques they apply. For risk identification and classification, the most common technique used was checklists, with a word count of four (30.8%), followed by interviews, with a word count of three (23.1%). For risk analysis, experience/judgement/intuition scored 11 word counts (85%), making it the most popular technique adopted by the firms. This is followed by sensitivity analysis with six word counts (46.1%), risk-adjusted discount rate (RADR) with three word counts (23.1%), and scenario technique with two word counts, representing 15.38% of the total firms. Finally, a greater percentage of the firms engaged in one form of risk response approach or the other; these include risk avoidance, transfer, mitigation, and acceptance. These findings are somewhat synonymous with the quantitative result (see Tables 6–8). Nonetheless, further probing revealed that none of the development firms applied probabilistic techniques such as value at risk, the Monte Carlo simulation, or algorithms. This contradicts the results presented in Table 7.

Few companies (15.38%) adopted well-formulated risk management strategies, such as the COSO (2004) Enterprise Risk Management Framework. This finding does not align with the quantitative results, in which over half (52%) of the companies claimed to have well-formulated risk management strategies. Interestingly, the UACN Property Development Company (UPDC), which is the only listed real estate development company in Nigeria (see Figure 3), had a well-structured risk management strategy adapted from the COSO framework. The firm had an established risk management culture that encompassed risk identification at every stage of the project, risk assessment and evaluation, risk monitoring, risk mitigation, and risk reporting. In contrast, 38.46% of the companies had a consistently defined risk catalogue for risk identification. A risk catalogue is a structured document listing potential risks that could affect project outcomes (PMBOK, 2017). This finding is consistent with the survey results.

Finally, the CEOs of small and medium-sized companies were mainly responsible for risk management, while in some cases, no staff member was directly assigned to the role. Large firms, such as UPDC, engage risk management experts or committees. These findings align with the quantitative results (see Figure 3). Overall, most of the qualitative findings correspond with the quantitative results, although some discrepancies exist. Both sets of findings suggest that the risk management techniques used by development companies are predominantly qualitative, with minimal adoption of probabilistic methods. The implication is that a gap exists between theory and practice in the Nigerian real estate development sector.

Discussion

Referencing both the qualitative interview findings and quantitative survey data, the results paint a comprehensive picture of the current risk analysis and management practices in Nigeria. Overall, the findings suggest that risk management practices in the Nigerian real estate development industry were largely characterised by the use of qualitative techniques, with limited adoption of sophisticated or quantitative methods. These findings are consistent with the outcomes of previous studies (Gehner et al., 2006; Otegbulu et al., 2011; Wiegelmann, 2012; Nnamani, 2017; Moorhead et al., 2021), which point to a maturing but still underdeveloped risk management culture, one that carries implications for the long-term sustainable growth and resilience of the sector.

One of the most remarkable findings from the quantitative survey was the predominance of basic, qualitative techniques for risk identification and classification. Brainstorming, checklist methods, and interviews were the most commonly used methods, with the influence diagram hardly adopted. These findings are consistent with the results of Uher and Toakley (1999).In contrast, checklist methods emerged as the most common risk identification technique in qualitative data, followed by interviews. These suggest a preference for experience-driven, intuitive techniques over systematic or data-driven ones. While brainstorming and checklists are important for initiating discussions and ensuring thoroughness, they lack the analytical depth provided by more sophisticated approaches such as influence diagrams or decision trees. The reliance on simpler tools can be attributed to a lack of technical capacity, limited training, or the apparent complexity of advanced techniques.

In terms of risk analysis, the survey results revealed a strong bias toward intuitive and experiential approaches. Techniques such as experience, judgement, and intuition dominated, while advanced tools like the Monte Carlo simulation and algorithmic methods were rarely used. Sensitivity analysis appears to be somewhat more commonly adopted, indicating a moderate effort to incorporate structured analysis. In the context of risk analysis, the dominance of experience/judgement/intuition in word frequency further supports the survey findings. Techniques such as sensitivity analysis, RADR, and scenario analysis were mentioned less frequently. These findings, which align with previous research (Wiegelmann, 2012; Nnamani, 2017), suggest that even among those familiar with quantitative methods, few apply them consistently. Furthermore, the predominance of experiential approaches indicates that data-driven modelling and structured evaluation are still not deeply embedded in the risk management practices of property development companies in Nigeria.

In terms of risk response, the quantitative findings indicate that risk avoidance was the most frequently adopted strategy, while risk transfer, such as through insurance, was the least utilised. This aligns with the qualitative findings but contrasts with earlier studies (Baker et al., 1999; Lyons & Skitmore, 2004), which showed that most firms engaged in a variety of risk response strategies, including avoidance, transfer, mitigation, and acceptance. The low rate of risk transfer suggests a reluctance or inability to utilise formal financial instruments like insurance. This may be attributed to factors such as cost, lack of trust in insurance institutions, or limited awareness of available products. The preference for risk avoidance over risk transfer has important implications. Risk avoidance typically involves steering clear of activities deemed too risky. While this can be a prudent strategy, excessive reliance on it may hinder innovation and restrict growth opportunities. In contrast, risk transfer mechanisms like insurance can empower firms to pursue larger and potentially more profitable projects while managing downside risk. The underutilisation of such tools highlights a potential area for policy intervention and industry-wide education.

While the majority of firms reported conducting FFA, it is important to note that many of them outsourced this process, particularly public developers. Only approximately one-third of firms could clearly articulate the tools used for FFA, with cash flow analysis and payback period being the most cited. This suggests that although FFA is practiced in name, its depth and rigor vary widely, and its outcomes may not be fully integrated into the decision-making process (Moorhead et al., 2021).

The survey also highlights significant gaps in the formalisation of risk management practices. Only approximately half of the firms reported having a well-formulated risk management strategy, while the rest did not. Moreover, just 39% of firms used a consistently defined risk catalogue. These figures underscore a broader issue: the absence of standardised procedures for risk identification, classification, and monitoring. Without these, firms are likely to miss or underestimate certain categories of risk, leading to poorly informed decision-making. The qualitative interviews highlight and contextualise these findings. Most notably, they reveal that many property development companies did not operate under a standard risk management framework. Only a few firms, such as UPDC, a publicly listed company, utilised structured frameworks such as the COSO Enterprise Risk Management Framework. UPDC’s practice, which includes risk identification, assessment, evaluation, monitoring, mitigation, and reporting at each stage of the project, represents a best-practice model. Its structured approach serves as a benchmark for other firms and demonstrates the value of institutionalised risk management processes.

The disparity between UPDC and smaller or medium-sized firms indicates a fragmentation in the industry’s maturity levels regarding risk management. While larger firms may have access to knowledge, resources, and regulatory expectations that support structured risk practices, smaller firms often operate with limited capacity and informal approaches. This was illustrated vividly in an interview with a sole-owner developer who stated that he does not believe in FFA or risk management, asserting that “once the location is right, the investment cannot fail.” Such a mindset underlines a fundamental misunderstanding of the role of risk analysis and reflects an overreliance on intuition and experience.

Another key finding is the limited use of comprehensive risk management systems. While firms like UPDC demonstrate what is achievable with a well-integrated approach, the broader landscape remains fragmented and inconsistent. This fragmentation could expose the industry to systemic risks, particularly in a volatile economic environment like Nigeria’s, where economic fluctuations, regulatory changes, and political instability are constant threats.

In summary, these results indicate that most of the risk management techniques applied were the very simple ones. The in-depth personal interviews also portrayed that there is a huge gap between theory and practice. The interviewee respondents have theoretical knowledge of some of the risk management techniques but did not put them into practice. Notwithstanding the high-risk development environment, developers mostly relied on subjective approaches to assess risks, while the implementation of robust risk management techniques remains limited. The application of subjective techniques, which frequently rely on subjective judgements, could result in inconsistencies and biases, potentially leading to misinterpretations in risk management decisions. Although the qualitative approaches have their limitations, they help appreciate some complex risks such as regulatory, stakeholders’ perception, and environmental issues that cannot be easily quantified. Nonetheless, combining qualitative approaches with quantitative methods, especially the Monte Carlo simulation, would create a comprehensive and more balanced risk management strategy in real estate development projects. Moreover, it could also be inferred from the results that the structural characteristics of the development firms play a key role in how they approach risk management. For example, UPDC, which has a comprehensive risk management framework, is the only listed development firm in Nigeria. Its approach to risk management can be accounted for by the organisational structure.

Conclusion

This study, which forms part of a broader study on risk management practices in Nigeria, assessed the risk analysis and management practices of real estate development companies across the six geopolitical zones of the country. An explanatory sequential mixed-methods design was employed to investigate the application of risk management techniques, drawing on responses from 84 survey participants and 13 interviewees. Using descriptive statistics to analyse 31 risk management techniques, the results indicate that brainstorming, checklists, experience/judgement/intuition, risk avoidance, and interviews were the most commonly adopted techniques by real estate developers in managing risks in development projects. While brainstorming, checklists, and interviews were classified under risk identification and classification, experience/judgement/intuition and risk avoidance were categorised under risk analysis and risk response, respectively. Although more than half of the development firms had well-formulated strategies for risk management, these did not consistently translate into practice. Fewer than half of the firms consistently defined the risk catalogue used for identification, while more than half did not. Regarding staff responsible for risk management, the chief executive officer accounted for approximately one-third of the cases, followed by the operations officer. Conversely, approximately one-fourth of the firms did not assign the role to any specific staff member, and only a few assigned it to a risk management expert or committee.

Thematic content analysis of the interview data validated several findings from the descriptive analysis. Additionally, a larger proportion of firms conducted FFA, and some adopted multiple risk management techniques in development decision-making. These findings suggest that most developers primarily relied on qualitative risk management techniques rather than quantitative ones, such as the Monte Carlo simulation. Nevertheless, some firms applied sensitivity analysis and scenario techniques, despite their limitations. Although qualitative methods can introduce inconsistencies and biases that may lead to misjudgements, they are useful for understanding complex, non-quantifiable risks. Therefore, combining qualitative and quantitative methods, especially probabilistic approaches, can offer a more comprehensive and balanced risk management framework for real estate development projects. The findings from this study can aid both local and international developers in making informed decisions regarding risk analysis and management in countries with characteristics similar to those of Nigeria. Moreover, the study contributes to the body of literature on real estate development risk in emerging markets. It is recommended that further research empirically examine the relationship between the structural characteristics of development companies and their risk analysis and management practices. Additionally, future studies should assess the factors influencing the adoption of risk management techniques by development firms, particularly within the context of emerging markets.

References

Adegboye, K. (2018, July 10). Abandoned housing projects litter Nigeria. Vanguard Newspapers. https://www.vanguardngr.com/2018/07/abandoned-housing-projects-litter-nigerian-cities/

Akintoye, A. S., & MacLeod, M. J. (1997). Risk analysis and management in construction. International Journal of Project Management, 15(1), 31–38. https://doi.org/10.1016/S0263-7863(96)00035-X

Alschuler, L. and Dawson, K.S. (2024). COSO Releases Enterprise Risk Management -Integrated Framework Authored by PricewaterhouseCoopers, Principles-Based Framework for Managements and Boards to Comprehensively Manage Risks to Objectives. Available at: https://www.icjce.es/images/pdfs/TECNICA/C03%20-%20AICPA/C309%20-%20Otras%20entidades/COSO%20-%20ERM%20-%20Execsum%20-%20Sept%202004.pdf. (Accessed 01 February 2025)

Association for Project Management. (2012). Association for Project Management Book of Knowledge (6th ed.). Association for Project Management.

Association for Project Management. (2019). Association for Project Management Book of Knowledge (7th ed.). Association for Project Management.

Ayodele, T. O., & Olaleye, A. (2021). Flexibility decision pathways in the management of uncertainty in property development: Experience from an emerging market. Journal of Financial Management of Property and Construction, 26(3), 408–432. https://doi.org/10.1108/JFMPC-05-2020-0037

Baker, S., Ponniah, D., & Smith, S. (1999). Survey of risk management in major UK companies. Journal of Professional Issues in Engineering Education and Practice, 125(3), 94–102. https://doi.org/10.1061/(ASCE)1052-3928(1999)125:3(94)

Baldi, F. (2013). Valuing a greenfield real estate property development project: A real options approach. Journal of European Real Estate Research, 6(2), 186–217. https://doi.org/10.1108/JERER-06-2012-0018

Banaitiene, N., Banaitis, A., & Norkus, A. (2011). Risk management in construction projects: Peculiarities of Lithuanian construction companies. International Journal of Strategic Property Management, 15(1), 60–73. https://doi.org/10.3846/1648715X.2011.568675

Baruch, Y., & Holtom, B. C. (2008). Survey response rate levels and trends in organizational research. Human Relations, 61(8), 1139–1160. https://doi.org/10.1177/0018726708094863

Berg, H. (2010). Risk management: Procedures, methods and experiences. RT&A, 1(June), 79–95. http://www.gnedenko-forum.org/Journal/2010/022010/RTA_2_2010-09.pdf

Bhoola, V., Hiremath, S. B., & Mallik, D. (2014). An assessment of risk response strategies practiced in software projects. Australasian Journal of Information Systems, 18(3), 161–191. https://doi.org/10.3127/ajis.v18i3.923

Braun, V., & Clarke, V. (2006). Using thematic analysis in psychology. Qualitative Research in Psychology, 3(2), 77–101. https://doi.org/10.1191/1478088706qp063oa

Byrne, P. (2002). Risk, uncertainty and decision-making in property development (2nd ed.). Routledge. https://doi.org/10.4324/9780203475515

Cameron, R. (2009). A sequential mixed model research design: Design, analytical and display issues. International Journal of Multiple Research Approaches, 3(2), 140–152. https://doi.org/10.5172/mra.3.2.140

Centre for Affordable Housing Finance in Africa. (2020). Nigeria’s housing construction and housing rental activities: Cost benchmarking and impact on the economy. Centre for Affordable Housing Finance in Africa. http://housingfinanceafrica.org/app/uploads/Nigeria-HEVC-Final-Report-June-2020-1.pdf

Chapman, C., & Ward, S. (2011). How to manage project opportunity and risk (3rd ed.). John Wiley & Sons. https://doi.org/10.1002/9781119208587

Creswell, J. W., & Creswell, J. D. (2018). Research design: Qualitative, quantitative, and mixed methods approaches (5th ed.). Sage Publications.

Crosby, N., Devaney, S., & Wyatt, P. (2020). Performance metrics and required returns for UK real estate development schemes. Journal of Property Research, 37(2), 171–193. https://doi.org/10.1080/09599916.2020.1720269

Debrah, C., Owusu-Manu, D. G., Amonoo-Parker, L., Baiden, B. K., Oduro-Ofori, E., & Edwards, D. J. (2022). A factor analysis of the key sustainability content underpinning green cities development in Ghana. International Journal of Construction Management, 23(14), 2469–2478. https://doi.org/10.1080/15623599.2022.2068786

Debrah, C., Owusu-Manu, D. G., Kissi, E., Oduro-Ofori, E., & Edwards, D. J. (2020). Barriers to green cities development in developing countries: Evidence from Ghana. Smart and Sustainable Built Environment, 11(3), 438–453. https://doi.org/10.1108/SASBE-06-2020-0089

Deloach, J. W. (2000). Enterprise-wide risk management: Strategies for linking risk and opportunity. Financial Times Prentice-Hall.

Fisher, P., & Robson, S. (2006). The perception and management of risk in UK office property development. Journal of Property Research, 23(2), 135–161. https://doi.org/10.1080/09599910600800484

Gehner, E. (2008). Knowingly taking risk: Investment decision making in real estate development. Eburon Academic Publishers.

Gehner, E., Halman, J. I. M., & de Jonge, H. (2006, April 6–7). Risk management in Dutch real estate development sector: A survey. 6th International Postgraduate Research Conference in the Built and Human Environment, Salford, United Kingdom. University of Salford.

Ghonegun, V., & Olorunlomeru, A. (2021, November 7). Lagos and burden of recurring collapse of structures. The Guardian. https://guardian.ng/sunday-magazine/lagos-and-burden-of-recurring-collapse-of-structures/

GleiBner, W., & Wiegelmann, T. (2012). Quantitative methods for risk management in the real estate development industry. Journal of Property Investment & Finance, 30(6). https://doi.org/10.1108/jpif.2012.11230faa.002

Hargitay, S. (1985). Selection of assets for a property portfolio using portfolio theory. Journal of Valuation, 3(3), 272–283. https://doi.org/10.1108/eb007977

Havard, T. (2014). Financial feasibility studies for property development: Theory and practice. Routledge. https://doi.org/10.4324/9780203640227

Isaac, D., O’Leary, J., & Daley, M. (2010). Property development: Appraisal and finance. Palgrave Macmillan. https://doi.org/10.1007/978-1-137-20172-0

Khedekar, S., & Dhawale, A. (2015). Qualitative risk assessment and mitigation measures for real estate projects in Maharashtra. International Journal of Technical Research and Applications, 3(4), 49–57. https://www.ijtra.com/view/qualitative-risk-assessment-and-mitigation-measures-for-real-estate-projects-in-maharashtra.pdf

Krejcie, R. V., & Morgan, D. W. (1970). Determining sample size for research activities. Educational and Psychological Measurement, 30(3), 607–610. https://doi.org/10.1177/001316447003000308

Kutsch, E., & Hall, M. (2010). Deliberate ignorance in project risk management. International Journal of Project Management, 28(3), 245–255. https://doi.org/10.1016/j.ijproman.2009.05.003

Kvale, S. (1996). Interviews: An introduction to qualitative research interviewing. Sage Publications.

Kvale, S., & Brinkmann, S. (2009). Interviews: Learning the craft of qualitative research interviewing. Sage Publications.

Liow, K. H. (2008). Extreme returns and value at risk in international securitized real estate markets. Journal of Property Investment & Finance, 26(5), 418–446. https://doi.org/10.1108/14635780810900279

Lizieri, C., & Finlay, L. (1995). International property portfolio strategies: Problems and opportunities. Journal of Property Valuation and Investment, 13(1), 6–21. https://doi.org/10.1108/14635789510146596

Loizou, P., & French, N. (2012). Risk and uncertainty in development: A critical evaluation of using Monte Carlo simulation method as a decision tool in real estate development projects. Journal of Property Investment & Finance, 30(2), 198–210. https://doi.org/10.1108/14635781211206922

Lyons, T., & Skitmore, M. (2004). Project risk management in the Queensland engineering construction industry: A survey. International Journal of Project Management, 22(1), 51–61. https://doi.org/10.1016/S0263-7863(03)00005-X

Makui, A., Mojtahedi, S. M., & Mousavi, S. (2010). Project risk identification and analysis based on group decision making methodology in a fuzzy environment. International Journal of Management Science and Engineering Management, 5(2), 108–118. https://doi.org/10.1080/17509653.2010.10671098

Mintah, K. (2018). Real options analysis in residential property development decision-making in Australia: Perspective of executives. International Real Estate Review, 21(4), 473–520. https://www.um.edu.mo/fba/irer/papers/past/vol21n4_pdf/03.pdf. https://doi.org/10.53383/100270

Moorhead, M., Armitage, L., & Skitmore, M. (2021). Risk management processes used in determining project feasibility in the property development process early stages by Australia/New Zealand property developers. Journal of Property Investment & Finance, 40(6), 628–642. https://doi.org/10.1108/JPIF-08-2021-0071

National Bureau of Statistics. (2021). Selected banking sector data: Sectorial breakdown of credit, e-payment channels and staff strength (Q4 2020). National Bureau of Statistics. https://nigerianstat.gov.ng/elibrary/read/1241018

Ng, S. T., Smith, N. J., & Skitmore, M. (1995). Case-based reasoning for contractor pre-qualification. In 4th International Conference on the Application of Artificial Intelligence to Civil and Structural Engineering. Development in artificial intelligence for civil and structural engineering.

Nnamani, O. C. (2017). Application of quantitative risk assessment techniques in property investment appraisal in Enugu urban, Nigeria. Journal of Land Management and Appraisal, 5(1), 23–41. https://academicjournals.org/journal/JLMA/article-full-text-pdf/DB9D3BE58643

Ogbuefi, J. U. (2002). Aspects of feasibility and viability studies. Institute of Development Studies, University of Nigeria, Enugu Campus.

Ogunba, O. A. (2002). Pre development appraisal and risk adjustment techniques in southwestern Nigeria (Doctoral dissertation). Obafemi Awolowo University.

Okafor, F. O. (2002). Sample survey theory with applications. Afro-Orbis Publishers.

Otegbulu, A. C., Mohammed, M. I., & Babawale, G. K. (2011). Survey on risk assessment techniques applied in real estate development project in Nigeria. Journal of Contemporary Issues in Real Estate, 1(1), 189–202.

Preller, F. T. (2009). A critical assessment of pre-construction property development principles and process in Queensland, Australia (Doctoral dissertation). Curtin University. https://espace.curtin.edu.au/handle/20.500.11937/1009

Project Management Institute. (2013). A guide to the Project Management Body of Knowledge (5th ed.). Project Management Institute.

Project Management Institute. (2017). A guide to the Project Management Body of Knowledge (PMBOK® Guide) (6th ed.). Project Management Institute.

Ratcliffe, J., Stubbs, M., & Keeping, M. (2021). Urban planning and real estate development (4th ed.). Taylor & Francis Group. https://doi.org/10.4324/9780429398926

Raz, T., & Michael, E. (2001). Use and benefits of tools for project risk management. International Journal of Project Management, 19(1), 9–17. https://doi.org/10.1016/S0263-7863(99)00036-8

Reed, R., & Sims, S. (2015). Property development (6th ed.). Routledge. https://doi.org/10.4324/9781315766652

Saidu, A. I., & Yeom, C. (2020). Success criteria evaluation for a sustainable and affordable housing model: A case for improving household welfare in Nigeria cities. Sustainability, 12(2), 656. https://doi.org/10.3390/su12020656

Taherdoost, H. (2016). Validity and reliability in research instrument: How to test the validation of a questionnaire/survey in a research. International Journal of Academic Research and Management, 5(3), 28–36. https://doi.org/10.2139/ssrn.3205040

Uher, T. E., & Toakley, A. R. (1999). Risk management in the conceptual phase of a project. International Journal of Project Management, 17(3), 161–169. https://doi.org/10.1016/S0263-7863(98)00024-6

Whipple, R. T. M. (1988). Evaluating development projects. Journal of Valuation, 6(3), 253–286. https://doi.org/10.1108/eb008029

Wiegelmann, T. W. (2012). Risk management in the real estate development industry: Investigations into the application of risk management concepts in leading European real estate development organisations (Doctoral dissertation). Bond University.

Zhang, L., Wu, X., Skibniewski, M. J., Zhong, J., & Lu, Y. (2014). Bayesian-network-based safety risk analysis in construction projects. Reliability Engineering & System Safety, 131, 29–39. https://doi.org/10.1016/j.ress.2014.06.006

Zou, Y., Kiviniemi, A., & Jones, S. W. (2017). Retrieving similar cases for construction project risk management using natural language processing techniques. Automation in Construction, 80, 66–76. https://doi.org/10.1016/j.autcon.2017.04.003