Construction Economics and Building

Vol. 23, No. 3/4

December 2023

RESEARCH ARTICLE

Effect of Anti-corruption Systems’ Logic on Corruption Manifestations in Project Planning and Execution in Nigeria

Olugboyega Oluseye1,*, Bobga Binga1, Oseghale Godwin Ehis1, Clinton Aigbavboa2

1 Faculty of Environmental Design and Management, Department of Building, Obafemi Awolowo University, Ile-Ife, Nigeria

2 cidb Centre of Excellence, University of Johannesburg, South Africa

Corresponding author: Olugboyega Oluseye, Faculty of Environmental Design and Management, Department of Building, Obafemi Awolowo University, Ile-Ife, Nigeria, oolugboyega@oauife.edu.ng

DOI: https://doi.org/10.5130/AJCEB.v23i3/4.8885

Article History: Received 27/01/2023; Revised 20/09/2023; Accepted 31/10/2023; Published 23/12/2023

Abstract

The absence of logical reasoning in the implementation of anti-corruption measures has exerted a significant influence, leading to misguided anti-corruption endeavours in nations such as Nigeria. The objective of this study is to discern the underlying rationale behind anti-corruption systems and ascertain their impact on the occurrence of corruption in the context of project planning and execution (PPE) within Nigeria. The research formulated a theoretical framework that classified the anti-corruption measures into three distinct systems and elucidated their underlying rationale. The model postulates that anti-corruption measures that exhibit a significant influence on corruption in the realm of PPE are those that prioritise the enhancement of reputation and remuneration. The hypotheses were extracted from the model and subjected to testing through the utilisation of multiple linear regression (MLR). The efficacy of all the classifications of anti-corruption systems was determined to be inadequate in mitigating the occurrence of bribery, fraud, and substandard documentation. The empirical findings indicate that the expansion of information access exhibits a robust logical framework and exerts a substantial influence on the prevalence of corruption within the realm of PPE in Nigeria. The results of this study propose a potential strategy for an anti-graft campaign and provide insights into the importance of consolidation.

Keywords

Anti-corruption Crusade in Nigeria; Anti-corruption Systems in Nigeria; Corruption in Construction Industry; Corruption in Nigeria

Introduction

The African Union Convention on Preventing and Combating Corruption and Related Offences established anti-corruption tactics and procedures (Mikail, et al., 2017; Mikail, 2018). Since the country was restored to civil rule in May 1999, the Nigerian government has launched a host of measures (for example, whistleblowing, watchdogs, and the Treasury Single Account) targeted at tackling corruption in various economic sectors (Inuwa, et al., 2019; Inuwa, Ononiwu and Kah, 2020). Since 1999, the impact of anti-corruption initiatives in the Nigerian construction sector has been uncertain. The existing literature focuses on the influence of anti-corruption strategies on corruption in the banking and political sectors (Nnadozie, 2021; Joseph, et al., 2016). These sectors are important to the socioeconomic growth of every country, but the construction industry is more basic to the economy and the activities of the other sectors in any country (Oladinrin, Ogunsemi and Aje, 2012; Erol and Unal, 2015). Despite the importance of the construction sector, existing anti-corruption studies have only reviewed anti-corruption practises in the construction sector and identified the potential of e-procurement (Mackey and Cuomo, 2020; Aduwo, et al., 2020; Afolabi, et al., 2020), technical auditing (Lehtinen, et al., 2022; Owusu, et al., 2019; Hetami and Aransyah, 2020; According to the findings of these investigations, corruption occurs most frequently during the project planning and execution stages, and current anti-corrupt practises are reactive rather than proactive.

As a result, there is a gap in analysing the effectiveness of anti-corruption measures in the construction industry. The main issue is that anti-corruption systems have been studied for effectiveness without considering their dimensional logic and logical focus (Lehtinen, et al., 2022; Oberoi, 2014; McCusker, 2006). This strategy is problematic since a single anti-corruption measure will be ineffective in combating corruption. Only by combining several anti-corruption measures can an effective anti-corruption system be established. Because there is no one-size-fits-all anti-corruption measure, each anti-corruption measure in the system should have a focus and priority in the fight against corruption (Lehtinen, et al., 2022). According to Oberoi (2014), little progress has been made in eradicating corruption as a result of faulty and misplaced anti-corruption campaigns done without reasoning. As a result, it is critical to define the various categories of anti-corruption systems and link their levels of logic to their levels of effectiveness for a practical assessment of their viability. The effectiveness of anti-corruption systems is best assessed during project planning and execution, which have been identified as the stages with the highest occurrence of corruption (Owusu, et al., 2019; Mackey and Cuomo, 2020).

The goal of this research is to foster conceptual understanding of anti-corruption systems that impact corruption in the construction sector by analysing the logic (focal points and rationale) of anti-corruption systems and establishing anti-corruption systems that satisfactorily and fundamentally address corruption in project planning and execution. To fulfil the study’s goal, the study identified and evaluated the rationale and effectiveness of anti-corruption systems on corruption in project planning and execution. This study is significant because it will aid in the identification of anti-corruption strategies that are typically feasible, significant, and compelling. The classification of the construction sector as the one with the highest level of corruption (Maruichi and Abe, 2019; Adekunle, et al., 2019) emphasises the importance of this investigation.

Literature review

Classifications and logic of anti-corruption systems

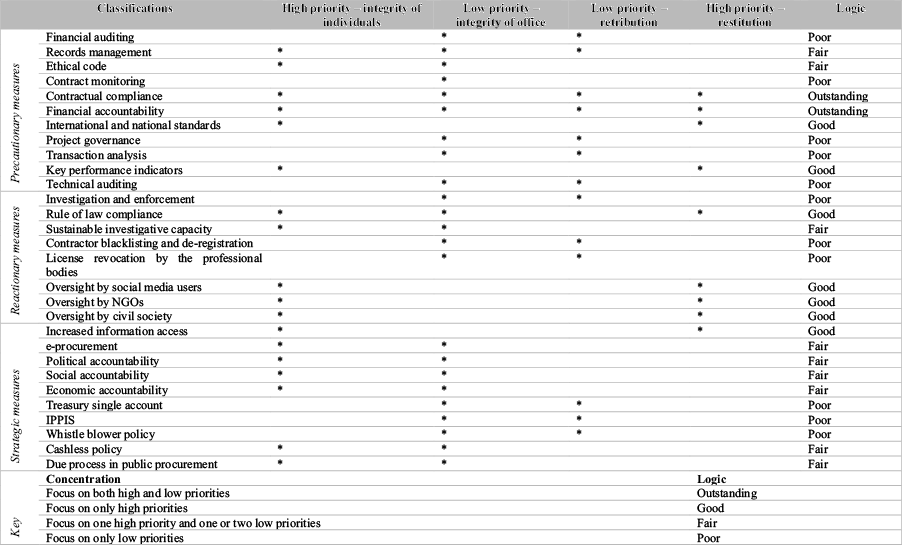

Scholars cannot agree on how anti-corruption systems should be classified; therefore, the argument continues (Badawi and Al-Qudah, 2019; Adnan, et al., 2012; Fan, et al., 2022; Zou, 2006; Owusu, et al., 2019). The categories were built on a number of assumptions. Interventionism, managerialism, and organisational schools of thought, for example, all hold that corruption stems from the organisation rather than the people who work inside it (Al-Hojjaj, 2020; McCusker, 2006). Based on the assumption that anti-corruption systems gain importance over time, they were further classified into three types: short-term, medium-term, and long-term systems (Badawi and Al-Qudah, 2019). Furthermore, these classifications provided little guidance for effective corruption management or the successful application of anti-corruption measures in the many various economic domains.

Before implementing an anti-corruption measure, studies recommend assessing its logic and viability (Lehtinen, et al., 2022; Oberoi, 2014). Oberoi (2014) claims that misdirected and untested anti-corruption initiatives have hindered corruption eradication. An effective anti-corruption system has dimensional logic as well as logical focus. This is because a single anti-corruption measure will not reduce corruption (Quah, 2013; Mackey and Cuomo, 2020; Afolabi, et al., 2020). A typical anti-corruption system should have at least three measurements, three logical foci, and three-dimensional logic (Oberoi, 2014). Effectiveness and anti-corruption system logic should be linked. In the following sub-sections, this study classifies anti-corruption methods and discusses their effectiveness in project planning and execution:

Logic of precautionary anti-corruption systems and their effects on corruption in project planning and execution

Preventative anti-corruption systems define a system in which preventative measures are taken to prevent corruption from occurring. Specific anti-corruption preventive methods have been recommended in the literature as effective in preventing corruption. Financial auditing, records management, ethical code, financial accountability, project governance, key performance indicators, and technical auditing are examples of these measures (Nnadozie, 2021; Omadjohwoefe, 2014; Joseph, et al., 2016; Rizk, Sobh and Hamzeh, 2018; Vian, 2020). The reasoning behind a precautionary anti-corruption system is primarily concerned with ensuring office integrity. Technical auditing, for example, is meant as an anti-corruption strategy to analyse both the feasibility and productivity of an organisation’s operations through free and objective confirmation (Hetami and Aransyah, 2020). This is why Sichombo, et al. (2009) advocated for the use of technical auditors early in the planning phase. The rationale of financial auditing can be found in Paterson, Changwony and Miller’s (2019) claim that greater emphasis should be paid to studying the human costs connected with illicit behaviour through regulatory disclosure and jurisprudential practise in the battle against corruption. By analysing the success of a wide range of players and activities in a project, key performance indicators serve as an anti-corruption tool (Ledeneva and Shekshnia, 2011).

Logic of reactionary anti-corruption systems and their effects on corruption in project planning and execution

Reactionary anti-corruption systems respond to corruption without preventing it. Reactionary anti-corruption systems include investigation and enforcement, rule of law compliance, sustainable investigative capacity, contractor blacklisting and de-registration, social media user oversight, and NGO oversight (Krastev, 2003; Zou, 2006; Sibanda, 2005; Mattoni and Odilla, 2021; Cartwright, Liu and Raddats, 2021). Reactionary anti-corruption strategies emphasise effective punishment for corruption and project delivery transparency (Jang, Park and Lee, 2012). For instance, Fan, et al. (2022) stated that the law and regulation enforcement system require all projects to go through the bidding process, tightens control over different types of projects, improves tendering management and supervision, and makes party interactions more transparent. Krastev (2003) called rule of law compliance the fastest route to anti-corruption compliance. Sibanda (2005) suggests professional groups blacklist, deregister, and revoke contractor licences to align anti-corruption strategies and campaigns. Social media users oversee individuals’ integrity by delivering information to the public to increase transparency and receptivity (Cartwright, Liu and Raddats, 2021; Mattoni and Odilla, 2021). By using freedom of information legislation to gain access to essential governmental services that would otherwise require bribery, NGOs improve transparency and integrity (Peisakhin and Pinto, 2010).

Logic of strategic anti-corruption systems and their effects on corruption in project planning and execution

Strategic anti-corruption systems predict corruption and choose the most crucial operational or political measures to combat it. Strategic anti-corruption systems usually involve collaboration, partnership, technology, policy change and development, capacity building, and systemic change. Anti-corruption scholars recommend whistleblower policy, cashless policy, e-procurement or e-government, due process in public procurement, increased information access, accountability (political, social, and economic), the Treasury Single Account (TSA) initiative, and the Integrated Payroll and Personnel Information System (IPPIS) for strategic anti-corruption systems (Ulain and Hussain, 2020; Folorunso and Simeon, 2021). Promoting openness and availability of information helps prevent corruption by enhancing office and individual integrity (Ulain and Hussain, 2020). By connecting citizens to their government digitally to obtain information and services, e-government boosts public officers’ integrity (Sheryazdanova and Butterfield, 2017). Political, social, and economic accountability allow citizens to hold politicians accountable through civic involvement, promoting transparency, accountability, and integrity (Hamilton-Hart, 2001). To protect public officials, the TSA combined government bank accounts, payments, and receipts (Bashir, 2016). IPPIS protects public personnel against corrupt risks in the former system or manual salary calculation (Folorunso and Simeon, 2021). Public procurement due process controls public construction projects and fights corruption in project planning and procurement, promoting procurement integrity (Ebekozien, 2020; Dza, et al., 2018). No anti-corruption system is all-encompassing. To improve and implement an anti-corruption system, its viability must be assessed (Quah, 2013). This study fills a significant research gap.

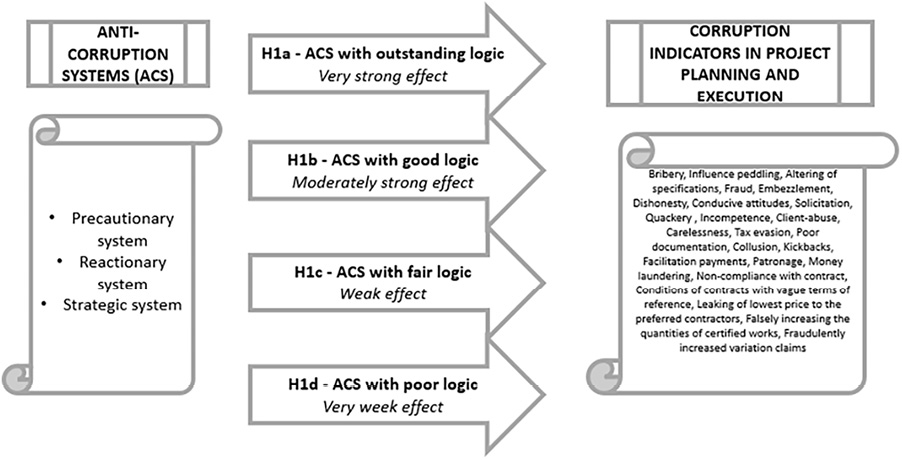

Research framework and hypothesis

Figure 1 depicts the theoretical model that underpins this research. The model suggests anti-graft system classifications and priorities. Anti-graft systems are classified as reactionary, precautionary, or strategic. Adnan, et al. (2012), Bertot, Jaeger and Grimes (2010), McCusker (2006), and Al-Hojjaj (2020) contend that the priorities of anti-graft systems are typically positioned on the enhancement of the integrity of officeholders (individuals or offices) and retribution (to discourage corruption) or restitution (to combat corruption). The model works by connecting the logic levels of anti-corruption systems to their levels of efficacy. The degrees of priority determine the levels of logic of an anti-corruption system (outstanding logic, good logic, fair logic, and poor logic). Priorities are divided into two categories: high priority (person integrity and reparation) and low priority (office integrity and retaliation). The logical focus of the anti-corruption system determines its level of efficacy. The model identifies four levels of effectiveness (very strong effect, moderately strong effect, weak effect, and very weak effect).

Figure 1. Classifications and logic of anti-corruption systems (source: figure formulated from Badawi and Al-Qudah, 2019; Fan, et al., 2022; Owusu, et al., 2019; McCusker, 2006; Lehtinen, et al., 2022)

Anti-corruption methods that focus on both high and low priorities are depicted to have excellent rationale and a very powerful effect on reducing corruption. Anti-corruption systems that focus solely on high priorities are regarded as having solid reasoning and a somewhat strong effect on corruption reduction. An anti-corruption strategy with a concentration on high priorities and one or two low priorities has a fair logic but a minimal effect on decreasing corruption. Anti-corruption programmes that focus solely on low-priority issues are regarded as having poor rationale and a negligible effect. The arguments of McCusker (2006), Quah (2013), Cartwright, Liu and Raddats (2021), Badawi and Al-Qudah (2019), Fan, et al. (2022), Al-Hojjaj (2020), Nnadozie (2021), and Rizk, Sobh and Hamzeh (2018) are used to establish the levels of logic and priorities of anti-corruption systems. According to McCusker (2006), encouraging rule-abiding behaviour would help people be disciplined and grasp what is expected of them and what will happen if the rules are broken.

Individuals who follow the rules are also able to be themselves and perform their tasks diligently. However, focusing on crime and retribution is a low-priority approach because it will only result in the imprisonment of corrupt persons and will only attack the symptoms of corruption (Quah, 2013; Al-Hojjaj, 2020; Lehtinen, et al., 2022). Such a system will have little impact because it reduces the anti-corruption component of punishment. This is because the corrupt individual appears to prioritise the potential of being detected over the punishment that could result from interception (Oberoi, 2014; Cartwright, Liu and Raddats, 2021). This means that, while fighting corruption and ensuring the integrity of public offices are important, a solid and effective anti-graft system would entail the development of a set of incentives to improve integrity by rewarding rule-abiding citizens and discouraging rule-aversion. It is logical to focus on the individuals who commit corrupt acts rather than the office or the actual corrupt conduct.

Thus, this study hypothesises that:

Hypotheses 1: There is an inverse relationship between anti-corruption systems’ logic and corruption manifestation in project planning and execution.

Hypothesis 1a (H1a): Anti-corruption systems with outstanding logic will have a very strong effect on corruption manifestations in project planning and execution.

Hypothesis 1b (H1b): Anti-corruption systems with good logic will have a moderately strong effect on corruption manifestations in project planning and execution.

Hypothesis 1c (H1c): Anti-corruption systems with fair logic will have a weak effect on corruption manifestation in project planning and execution.

Hypothesis 1d (H1d): Anti-corruption systems with poor logic will have a very weak effect on corruption manifestation in project planning and execution.

The hypothesised relationships in the hypotheses are summarised in Figure 2. The main hypothesis, as shown in Figure 2, illustrates that there is an inverse relationship between anti-corruption systems and corruption manifestations in project planning and execution. This hypothesis is based on the insights from Oberoi (2014), McCusker (2006), and Rizk, Sobh and Hamzeh (2018).

Methods

The study focuses on the construction industry in Nigeria; hence the study population are construction stakeholders (architect, builder, mechanical engineer, electrical engineer, quantity surveyor, town planner, and structural/civil engineer) in Lagos State, Nigeria. The study’s sample size was determined by randomly selecting the research participants from each of the professional categories. This gives a total sample size of 181. This sample size is considered appropriate because the rule of thumb for establishing the permissible sample size for multiple linear regression states that at least 10 observations per variable should be included (VanVoorhis and Morgan, 2007). This study has four major variables, resulting in a sample size of at least 40 people.

Random sampling technique was preferred to other techniques because it is free from bias, easy to implement, enables the making of statistical inferences about a population, helps ensure high internal validity, and allows all the units in the population to have an equal chance of being selected (Etikan and Bala, 2017). The social-demographic variables of the research participants included profession (architect – 15.7%, builder – 31.5%, mechanical engineer – 13.5%, electrical engineer – 6.7%, quantity surveyor – 13.5%, town planner – 9%, structural/civil engineer – 10%), education level (PhD – 2.2%, MSc – 24.7%, BSc – 42.7%, HND – 24.7%), experience (less than 5 years – 24.7%, 5-10 years – 33.7%, 11 – 15 years – 34.8%, 16 years and above – 6.7%), and projects participation (less than 5 projects – 33.7%, 5 – 10 projects – 30.3%, 11-15 projects – 20.2%, 16-20 projects – 6.7%, more than 21 projects – 9%).

Anti-corruption systems and corruption manifestation in project planning and execution are the main constructs for this study. Twenty-four (24) indicators were used to measure corruption manifestation in project planning and execution, while the anti-corruption system was divided into three subconstructs, namely, precautionary, reactionary, and strategic systems. The indicators for corruption manifestations were adopted from Olugboyega, et al., (2023). The anti-corruption systems were formulated from the anti-corruption measures identified from Fan, et al. (2022), Bertot, Jaeger and Grimes, (2010), Nnadozie (2021), and Owusu, et al. (2019). Precautionary systems were measured using eleven (11) variables, reactionary systems were measured using eight (8) variables, and strategic systems were measured using ten (10) variables. The measured variables for these subconstructs are presented in Table 2.

The questionnaire was subjected to content validation prior to the survey by delivering it to twelve subject specialists, who examined the contents of the questionnaire items to see if they represented the whole theoretical construct of the planned model of the problem under examination. Sixteen postgraduate students were also used to pilot-test the questionnaire. The professionals and postgraduate students completed the survey and provided feedback to help enhance the questionnaire. The internal consistency of the items in the questionnaire was verified using Cronbach’s Alpha to see if the items were consistent. The value of Cronbach’s alpha ranged between 0.77 to 0.89. Taber (2018) considers this range to be acceptable. The questionnaire survey to test the hypotheses was self-administered to a random sample of 181 construction stakeholders in Lagos State, Nigeria. The questionnaire was divided into three fundamental areas: the sociodemographic profile of respondents, corruption manifestations in project planning and execution, and anti-corruption systems impacting the corruption manifestations. Respondents were approached to offer their viewpoints as per the inquiries, adhering to the instructions given in each part.

Multiple linear regression (MLR) was utilised to test the hypotheses. The hypotheses were accepted or rejected based on their nature (positive or negative). Only hypotheses with a negative coefficient are acceptable because the hypotheses, as stated in Section 2.2, suggest an inverse relationship between anti-corruption systems’ logic and corruption manifestation in project planning and execution. The strength of the significance of the hypotheses was determined, as recommended by Evans (1996), as follows: very weak significance (0.00–0.19), weak significance (0.20–0.39), moderate significance (0.40–0.59), strong significance (0.60–0.79), and very strong significance (0.80 and above). MLR was selected for data analysis because it allows the assessment of the strength of the relationship between an outcome (the dependent variable) and several predictor variables as well as the importance of each of the predictors to the relationship. MLR is effective in determining the effect of each of the explanatory variables on the response variable and predicting the value of the response variable for a given value of explanatory variable (Maxwell, 2000). Before conducting the MLR, the anti-corruption systems and corruption indicators in project planning and execution were tested for reliability and significance. Table 1 presents the results of the reliability test. Formal testing such as tolerance, Variance Inflation Factor (VIF), and Durbin-Watson tests were conducted to recognise the presence of multicollinearity issues in the variables.

VIF is useful in solving multicollinearity in a regression analysis and identifying which variables are contributing to the multicollinearity. The higher the VIF value for a variable, the more it contributes to multicollinearity (Maxwell, 2000). Removing variables with high VIF values can help reduce multicollinearity and improve the accuracy and stability of the regression model. Tolerance describes the proportion of the variance of a variable in the equation that is not accounted for by other independent variables in the equation. It measures the influence of one independent variable on all other independent variables (Turner, 2020). The Durbin Watson test checks for auto correlation in the residuals of a statistical regression analysis. If auto correlation exists, it undervalues the standard error and may cause the researcher to believe that predictors are significant when in reality they are not (Turner, 2020).

Results

Data reliability and significance tests

According to the information presented in Table 1, none of the VIF values are greater than 10, while all of the tolerance results are greater than 0. This demonstrates that the anti-corruption systems are able to explain the symptoms of corruption to a large degree. The findings of the tolerance test reveal the degree to which the beta coefficients used in the regression model are impacted by the anti-corruption systems contained inside the model. The findings of the Durbin-Watson test indicate that a range of 1.50 to 2.50 is considered acceptable. This is in line with the recommendations of Turner (2020). This suggests that the variables do not exhibit any first-order autocorrelation with one another. According to the findings, the model does not suffer from a true case of multicollinearity, and the measured variables are found to be objective, consistent, and reliable for MLR. Table 2 presents the findings of a significance test that was run using the mean scores on the items in the survey. Because each of the factors has a mean score that is higher than 3.21, it can be deduced that they all have a very significant impact on the outcome.

Logic of precautionary anti-corruption systems and their effects on corruption in project planning and execution

The effects of precautionary anti-corruption systems (PACS) logic on corruption in project planning and execution are presented in Table 3. As demonstrated in the data, the PACS has a substantial impact on manifestations of corruption during project planning and execution. PACS with outstanding logic (contractual compliance and financial accountability) have a significant impact on corruption manifestations during project planning and execution. This lends credence to hypothesis 1a. PACS with good logic (international and national standards and KPIs) has a moderate effect on corruption manifestations during project planning and execution. This supports hypothesis 1b. It was discovered that PACS with poor logic (financial auditing, contract monitoring, project governance, transaction analysis, and technical auditing) had a negligible impact on the manifestation of corruption in project planning and execution. This supports hypothesis 1d. A PACS with fair logic includes record management and a code of ethics. In accordance with hypothesis 1c, they were found to have a minimal effect on corruption manifestation during project planning and execution.

β1=financial auditing; β2=records management; β3=ethical code; β4=contract monitoring; β5=contractual compliance; β6=financial accountability; β7=international and national standards; β8=project governance; β9=transaction analysis; β10=KPIs; β11=technical auditing

In addition, the table revealed that ethical code has a highly significant and negative effect on changing specifications (r = -1.032, p = 0.000) and money laundering (r = -0.924, p = 0.000). The correlation between technical auditing and embezzlement is statistically significant and negative (r = -0.843, p = 0.000). There was an inversely significant relationship between financial accountability and altering of specifications (r = -0.772, p = 0.000), solicitation (r = -0.629, p = 0.000), client abuse (r = -0.630, p = 0.000), facilitation payment (r = -0.708, p = 0.000), and fraud (r = -0.705, p = 0.000). The correlation between key performance indicators and embezzlement (r = -0.776, p = 0.000) and money laundering (r = -0.661, p = 0.000) The relationship between ethical code and carelessness (r = -0.660, p = 0.000), tax evasion (r = -0.621, p = 0.000), kickbacks (r = -0.688, p = 0.001), and conditions of contracts with imprecise terms of reference (r = -0.623, p = 0.001) is unambiguously and negatively correlated. The relationship between influence peddling and international and national standards is robust and negative (r = -0.689, p = 0.000).

International and national standards have a moderately negative relationship with modifying specifications (r = -0.427, p = 0.000), solicitation (r = -0.501, p = 0.000), carelessness (r = -0.458, p = 0.000), falsely increasing the quantities of certified works (r = -0.415, p = 0.000), and fraudulently increasing variation claims (r = -0.450, p = 0.000).A moderately negative relationship exists between financial accountability and embezzlement (r = -0.548, p = 0.000), conducive attitudes (9r = -0.450, p = 0.004), incompetence (r = -0.424, p = 0.000), negligence (r = -0.591, p = 0.000), and kickbacks (r = -0.433, p = 0.001). Technical auditing is moderately and negatively associated with negligence (r = -0.593, p = 0.000), facilitation payment (r = -0.591, p = 0.000), and patronage (r = -0.544, p = 0.000), as shown in the table. While dishonesty and contractual compliance have a moderately negative relationship with embezzlement (r = -0.494, p = 0.001), ethical code and contract monitoring have a moderately negative relationship with embezzlement (r = -0.533, p = 0.000). Ethical code was found to be negatively and moderately related to client abuse (r = -0.532, p = 0.000), while KPI was found to be negatively and moderately related to incompetence (r = -0.450, p = 0.000). Governance of a project has a moderately negative correlation with both quackery (r = -0.507, p = 0.000) and contract non-compliance (r = -0.594, p = 0.000).

Logic of reactionary anti-corruption systems and their effects on corruption in project planning and execution

As shown in Table 4, among the reactionary anti-corruption systems (RACS) with a good logic, oversights by NGOs are the only ones that have a relatively strong effect on the manifestations of corruption in project planning and execution, which lends support to hypothesis 1b. Despite having good logic, rule of law compliance, oversight by social media users, and oversight by civil society did not have a fairly substantial effect on the manifestations of corruption in project design and execution. RACS with fair logic (sustainable investigative capacity) has only a marginal impact on the manifestations of corruption in project planning and execution. This lends credence to hypothesis 1c by providing support for it. RACS with poor logic (investigation and enforcement, contractor blacklisting and de-registration, and license revocation) have a very limited impact on the manifestation of corruption in project planning and execution. This provides support for hypothesis 1d.

Table 4 displays the interrelationships between reactionary anti-corruption systems (RACS) and corruption manifestations in project planning and implementation. The relationship between contractor blacklisting, deregistration, and tax evasion is significant and negative, as shown in the table (r = -0.835, p = 0.000). There is a strong negative correlation between NGO oversight and changing specifications (r = -0.618, p = 0.000), dishonesty (r = -0.701, p = 0.000), client abuse (r = -0.614, p = 0.000), negligence (r = -0.661, p = 0.000), and favouritism (r = -0.603, p = 0.000). The table revealed that contractor blacklisting and de-registration are strongly and negatively associated with solicitation (r = -0.723, p = 0.000), kickbacks (r = -0.596, p = 0.000), and conditions of contracts with ambiguous terms of reference (r = -0.536, p = 0.000).

There was a moderately negative association between contractor blacklisting and specification alteration (r = -0.471, p = 0.000) and dishonesty (r = -0.337). The correlation between oversight by NGOs and embezzlement (r = -0.557, p = 0.000), a conducive attitude (r = -0.483, p = 0.000), collusion (r = -0.464, p = 0.000), money laundering (r = -0.509, p = 0.000), and conditions of contracts with vague terms of reference (r = -0.579, p = 0.000) was moderately negative. The relationship between sustainable investigative capacity and facilitation payments was moderately negative (r = -0.407, p = 0.000). The table reveals that all RACS have a very tenuous relationship with at least one manifestation of corruption in project planning and execution. Civil society oversight is only marginally and negatively associated with contract noncompliance (r = -0.079, p = 0.000).

β1=investigation and enforcement; β2=rule of law compliance; β3=sustainable investigative capacity; β4=contractor blacklisting and de-registration; β5=license revocation; β6=oversight by social media users; β7=oversight by NGOs; β8=oversight by civil society

Logic of strategic anti-corruption systems and their effects on corruption in project planning and execution

Table 5 shows the MLR analysis of the relationship between the logic of strategic anti-corruption systems (SACS) and corruption manifestations in project planning and execution. SACS with good logic (increased information access) has a minor impact on corruption manifestations during project planning and execution. This supports hypothesis 1b. SACS with fair logic (e-procurement, political accountability, social accountability, economic accountability, cashless policy, and due process in public procurement) have a minimal impact on the manifestation of corruption during project planning and execution. This supports hypothesis 1c. Treasury single account, Integrated Payroll and Personnel Information System (IPPIS), and whistleblower policy are SACS with poor logic. The result shows that they have a negligible impact on the manifestation of corruption in project planning and execution. This supports hypothesis 1d.

| Corruption manifestations | β1 | β2 | β3 | β4 | β5 | β6 | β7 | β8 | β9 | β10 | p-value |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Bribery | -0.245 | 0.049 | 0.212 | 0.014 | 0.068 | 0.300 | 0.034 | 0.271 | 0.055 | 0.060 | 0.002 |

| Influence peddling | -0.342 | 0.357 | -0.044 | 0.152 | -0.061 | 0.503 | -0.227 | -0.071 | 0.537 | 0.014 | 0.000 |

| Altering of specifications | -0.309 | 0.070 | 0.304 | 0.098 | 0.169 | 0.247 | 0.393 | 0.523 | 0.434 | -0.149 | 0.000 |

| Fraud | 0.002 | -0.148 | 0.065 | 0.068 | -0.024 | 0.438 | -0.031 | 0.256 | 0.052 | -0.009 | 0.000 |

| Embezzlement | 0.234 | -0.287 | -0.552 | 0.551 | 0.501 | 0.248 | 0.372 | 0.035 | 0.789 | 0.219 | 0.000 |

| Dishonesty | -0.486 | 0.177 | 0.021 | 0.255 | 0.224 | 0.206 | -0.115 | 0.479 | 0.477 | -0.264 | 0.004 |

| Conducive attitudes | -0.862 | 0.284 | 0.228 | -0.071 | -0.164 | 0.411 | 0.179 | 0.297 | 0.103 | 0.181 | 0.000 |

| Solicitation | 0.071 | -0.016 | 0.574 | -0.178 | -0.110 | 0.337 | -0.186 | -0.177 | -0.346 | -0.067 | 0.000 |

| Quackery | 0.075 | -0.164 | 0.146 | 0.053 | 0.315 | 0.297 | -0.214 | 0.034 | -0.613 | -0.107 | 0.000 |

| Incompetence | -0.030 | 0.026 | 0.195 | 0.030 | 0.357 | 0.116 | 0.172 | 0.138 | -0.283 | 0.052 | 0.000 |

| Client-abuse | -0.461 | 0.222 | 0.706 | -0.287 | 0.068 | 0.907 | -0.279 | 0.507 | 0.013 | -0.393 | 0.000 |

| Carelessness | -0.194 | 0.009 | 0.317 | 0.076 | 0.378 | 0.273 | 0.246 | 0.431 | 0.467 | -0.430 | 0.000 |

| Tax evasion | -0.377 | 0.219 | 0.789 | -0.719 | 0.580 | -0.178 | 0.284 | 0.256 | -0.420 | 0.219 | 0.000 |

| Poor documentation | -0.149 | -0.120 | -0.056 | 0.166 | 0.394 | 0.214 | 0.294 | 0.156 | 0.287 | -0.259 | 0.000 |

| Collusion | -0.280 | 0.186 | -0.484 | 0.278 | 0.063 | 0.182 | 0.307 | 0.201 | 0.205 | 0.018 | 0.001 |

| Kickbacks | -0.662 | 0.387 | 0.413 | -0.108 | 0.346 | 0.442 | 0.386 | 0.075 | 0.319 | 0.071 | 0.000 |

| Facilitation payments | -0.335 | 0.015 | 0.288 | -0.095 | 0.048 | 0.470 | -0.096 | 0.426 | -0.122 | 0.259 | 0.000 |

| Patronage | -0.225 | -0.103 | -0.186 | 0.139 | 0.166 | 0.700 | 0.023 | 0.134 | 0.491 | 0.198 | 0.000 |

| Money laundering | -0.453 | 0.351 | -0.016 | 0.242 | 0.523 | 0.448 | -0.077 | 0.757 | 0.646 | -0.347 | 0.000 |

| Non-compliance with contract | 0.230 | 0.094 | 0.286 | -0.075 | 0.251 | 0.545 | -0.216 | -0.091 | -0.046 | -0.347 | 0.000 |

| Conditions of contracts with vague terms of reference | -0.679 | 0.010 | 0.677 | -0.347 | 0.245 | 0.119 | 0.131 | 0.756 | -0.311 | -0.239 | 0.001 |

| Leaking of lowest price to the preferred contractors | -0.506 | 0.029 | 0.123 | 0.024 | 0.409 | 0.057 | 0.074 | 0.505 | 0.349 | 0.039 | 0.000 |

| Falsely increasing the quantities of certified works | -0.146 | -0.047 | 0.204 | -0.332 | 0.258 | -0.275 | 0.371 | 0.289 | 0.108 | -0.523 | 0.000 |

| Fraudulently increased variation claims | -0.609 | -0.011 | 0.053 | 0.049 | 0.021 | 0.365 | 0.132 | 0.203 | 0.230 | -0.345 | 0.000 |

| Logic | Good | Fair | Fair | Fair | Fair | Poor | Poor | Poor | Fair | Fair | |

| Support for hypothesis | Support H1b | Support H1c | Support H1c | Support H1c | Support H1c | Support H1d | Support H1d | Support H1d | Support H1c | Support H1c |

As shown in the table, there was an extremely significant and negative association between increased information access and solicitation (r = -0.862, p = 0.000); increased information access was also found to have a strong negative association with kickbacks (r = -0.662, p = 0.000), conditions of contracts with vague terms of reference (r = -0.679, p = 0.000), and fraudulently increased variation claims (r = 0.609, p = 0.000). There was a moderately negative correlation between increased information access and dishonesty (r = -0.486, p = 0.000), client abuse (r = -0.461, p = 0.000), money laundering (r = -0.453, p = 0.000), and disclosing the lowest price to preferred contractors (r = -0.506, p = 0.000). The correlation between cashless policy and quackery (r = -0.613, p = 0.000) and between social accountability and tax evasion (r = -0.719, p = 0.000) was determined to be overwhelmingly negative. A moderately negative relationship occurred between political accountability and embezzlement (r = -0.552, p = 0.000), increased information access and dishonesty (r = -0.486, p = 0.000), due process and carelessness (r = -0.430, p = 0.000), cashless policy and tax evasion (r = -0.420, p = 0.000), political accountability and collusion (r = -0.484, p = 0.000), and due process and falsely increasing the quantities of certified works (r = -0.523, p = 0.000).

β1=increased information access; β2=e-procurement; β3=political accountability; β4=social accountability; β5=economic accountability; β6=treasury single account; β7=IPPIS; β8=whistle blower policy; β9=cashless policy; β10=due process in public procurement

Discussion

Logic of precautionary anti-corruption systems (PACS) and their effects on corruption in project planning and execution

In the theoretical framework, this study proposed that anti-graft systems that successfully impact corruption in project planning and execution are those that focus on improving the uprightness of people and restitution. The proposition was tested using four sub-hypotheses. The findings from the hypothesis testing revealed that among the PACS, contractual compliance, financial accountability, KPIs, and adherence to international and national standards totally satisfied the conditions of the hypothesis. Also, the findings revealed that financial auditing, records management, the ethical code, contract monitoring, technical auditing, transaction analysis, and project governance totally satisfied the conditions of the hypothesis. The conditions of Hypotheses 1c and 1d were sufficiently met by investigation and enforcement, sustainable investigative capacity, contractor blacklisting and de-registration, and licence revocation.

As far as logic is concerned, the findings suggest that KPIs and adherence to international and national standards are exceptionally compelling PACS with outstanding rationale. Additionally, it is suggested in the findings that contractual compliance and financial accountability are extremely effective PACS with extraordinary rationale. This implies that these PACS should be prioritised in project planning and execution. For the most part, the findings revealed that none of the PACS is strong against bribery in project planning and execution. It was revealed from the findings that every one of the PACS is effective as anti-corruption measures in project planning and execution. Ethical codes, KPIs, technical auditing, and financial accountability are the most effective PACS for combating corruption manifestations in project planning and execution. Contractual compliance, adherence to international and national standards, project governance, and contract monitoring are also tolerably effective.

It could be inferred from these discoveries that professional ethics will forestall the altering of specifications and money laundering that are associated with project planning and execution (Adnan, et al., 2012). It very well may be accepted from the discoveries of this study that ethical building contractors wouldn’t be indiscreet in their obligations and commitments and wouldn’t dodge tax (Kuoribo, et al., 2021). The findings additionally propose that an ethical code would be viable in forestalling demand for kickbacks by public procurement officers or the inclusion of obscure terms of reference in contract agreements. An ethical code would also reduce client abuse, but its impact on misappropriation would be limited (Nelson and Afonso, 2019). Contract monitoring additionally and limitedly affects embezzlement. This is entirely avoidable through technical means. The findings infer that technical auditing would only modestly affect patronage, carelessness, and facilitation payments. The findings also infer that it would be nearly impossible to embezzle project funds, assuming a project is intended to have KPIs. Likewise, it shows from the findings that a project that is planned with KPIs and that has a project governance structure set up has decent potential for success in diminishing quackery and expanding contract compliance.

As inferred from this study’s findings, demanding financial accountability in project planning and execution could modestly decrease misappropriation of project funds, conducive attitudes of procurement and monitoring officers, incompetence and recklessness on the part of contractors, and the giving of kickbacks. Likewise, it appears that financial accountability in project planning and execution will keep contractors from soliciting contract awards, paying project procurement officers to lean towards them during pre-qualification, cheating clients, and changing qualifications to maximise profits (Jang, Park and Lee, 2012; Mackey and Cuomo, 2020; Paterson, Changwony and Miller, 2019). According to this study’s findings, a project that adheres to international and national standards would not encounter influence peddling from unqualified contractors. The findings uncovered that a method for preventing the altering of specifications and solicitation of contracts by unqualified and inept contractors is to specify the utilisation of international and national standards in the project plan (Lehtinen, et al., 2022). Apparently, projects that are planned and executed to standards (international and national) would record fewer variation claims and falsifications of certified works. The findings made it known that contractual compliance could lessen dishonesty to some degree, but it does not necessarily guarantee honesty on the part of contractors. It is possible that the findings of this study will lead to the discovery of payments made by contractors to facilitate the award of public contracts, assuming that the public procurement or anti-corruption agency has long-term investigative capacity.

Logic of reactionary anti-corruption systems (RACS) and their effects on corruption in project planning and execution

In Figure 1, none of the RACS was theorised as having a remarkable rationale, and none was found to satisfy Hypothesis 1a. Oversight by NGOs totally satisfied the conditions of Hypothesis 1b. The rule of law, oversights by social media users, and oversight by civil society failed to satisfy the conditions of Hypothesis 1b. This likewise goes against the positions of Cartwright, Liu and Raddats (2021) and Owusu, et al. (2019). In the theoretical framework, it was anticipated that the rule of law, oversight by social media users, and oversight by civil society would have outstanding logic and would be profoundly successful in battling corruption manifestations in project planning and execution. The outcomes nullified this proposition. Oversight by NGOs was found to be profoundly proficient and to have outstanding logic. This proposes that oversight by NGOs is a significant RACS.

Contractor blacklisting and de-registration are very effective against tax evasion, kickbacks, and solicitation among RACS. Oversight by NGOs weakly affects bribery. All other RACS are significantly weak against bribery. As suggested by the findings, the effect of oversight by NGOs on bribery and its striking impact on altering specifications, dishonesty, client abuse, carelessness, patronage, money laundering, conducive attitudes, and embezzlement make it the most valuable and compelling RACS. Shockingly, the findings revealed that oversight by social media users and civil society has an exceptionally limited impact in the fight against corruption in project planning and execution. This contradicts the position of Cartwright, Liu and Raddats (2021). The weak effect of social media users’ oversight on manifestations of corruption could be due to its abusive use. However, social media users’ oversight of manifestations of corruption could help raise awareness about the fight against corruption.

The findings shockingly revealed that the rule of law was of no significance in lessening corruption in project planning and execution. This depicts a critical disdain for the rule of law in Nigeria (Mikail, et al., 2017; Mikail, 2018; Inuwa, et al., 2020). The findings likewise made it known that blacklisting and de-registering contractors would dissuade them from evading tax. Additionally, manifestations of corruption like solicitation and kickbacks could be deterred in public project planning and execution by blacklisting and de-registering contractors that engage in these corrupt acts. Somewhat, as shown by the discoveries, blacklisting contractors that were dishonest and altered specifications on past projects would assist in decreasing the future occurrence of such degenerate acts among contractors (Hetami and Aransyah, 2020). The findings revealed that NGOs should be permitted to supervise the planning and execution of public projects, as this would assist with adjusting contractors’ efforts to alter project specifications, disparage public officers, abuse privileges and clients’ rights, and participate in reckless and unscrupulous acts. Also, oversights of public projects by NGOs would respectably diminish embezzlement, collusion, conducive attitudes, and money laundering (Tacconi and Williams, 2020).

Logic of strategic anti-corruption systems (SACS) and their effects on corruption in project planning and execution

Increased information access adequately satisfied the conditions of Hypothesis 1b. This suggests that increased information access is the best SACS. The Treasury Single Account, IPPIS, and whistleblower policy satisfactorily satisfied the conditions of Hypothesis 1d. The conditions of Hypothesis 1c were completely met by e-procurement, political accountability, social accountability, economic accountability, a cashless policy, and due process. As anticipated in the framework, increased information access was found to be the best SACS. Cashless policy, due process, social accountability, and political accountability were proposed as having fair logic; however, they were found to be compelling in combating manifestations of corruption in project planning and execution. This contradicts the positions of Owusu, et al. (2019), Lehtinen, et al. (2022), Mackey and Cuomo (2020), Afolabi, et al. (2020), Hetami and Aransyah (2020), and Sichombo, et al. (2009).

In the SACS classification, the weak association between increased information access and bribery suggested that increased information access is the only SACS that is helpful in the battle against bribery. The effects of the whistleblower policy and the Treasury Single Account on manifestations of corruption in project planning and execution were exceptionally weak and restricted to tax evasion, falsely increasing the quantities of certified works, influence peddling, solicitation, and non-compliance with contracts. The findings additionally demonstrated that every one of the SACS is valuable as anti-corruption measures in project planning and execution, but increased information access is the most useful system (Dza, et al., 2018; Aduwo, et al., 2020). Strategic measures that would altogether lessen manifestations of corruption in project planning and execution are increased information access, a cashless policy, due process, and political accountability. Increased information access, as demonstrated by the findings, would decisively forestall kickbacks, conditions of contracts with vague terms of reference, increased variation claims, solicitation, dishonesty, money laundering, and the leaking of the lowest price to the preferred contractor. A cashless policy would sufficiently guarantee social accountability and prevent tax evasion (Afolabi, et al., 2020). To a moderate degree, political accountability will decisively lessen collusion and embezzlement. With due process, there is a chance to tolerably forestall imprudence in project planning and execution.

Conclusions

This study investigated the inverse relationship between anti-corruption systems’ logic and corruption manifestations in project planning and execution. Based on the findings, the study’s proposition that anti-corruption systems with outstanding logic have a very strong effect on corruption manifestations in project planning and execution was met by PACS (contractual compliance and financial accountability). The postulation that anti-corruption systems with good logic have a moderately strong effect on corruption manifestations in project planning and execution was fulfilled by PACS (international and national standards and KPIs), RACS (oversight by NGOs), and SACS (increased information access). The hypothesis that anti-corruption systems with fair logic have a weak effect on corruption manifestation in project planning and execution was met by PACS (records management and ethical code), RACS (sustainable investigative capacity), and SACS (e-procurement, political accountability, social accountability, economic accountability, cashless policy, and due process in public procurement). The postulation that anti-corruption systems with poor logic have a very weak effect on corruption manifestation in project planning and execution was fulfilled by PACS (financial auditing, contract monitoring, project governance, transaction analysis, technical auditing), RACS (investigation and enforcement, contractor blacklisting and de-registration, licence revocation), and SACS (IPPIS, whistleblower policy, Treasury single account).

Thus, this study concludes that PACS are more effective than RACS and SACS. PACS would unequivocally impact corruption manifestations in the construction sector. These systems would fundamentally decrease corruption in the construction sector whenever they were joined with RACS and SACS with good logic, such as oversight by NGOs and increased information access. Increased information access was established as an anti-corruption system that is logically good since it centres around improving the integrity of individuals and restitution and would affect corruption in project planning and execution. Considering the effectiveness of oversight by NGOs in combating corruption, this study recommends that the independence and accountability of NGOs be upgraded. Every one of the classifications of anti-corruption systems is not effective against bribery, fraud, or poor documentation. Future examinations should research ways of tending to these corrupt acts in the construction sector.

This study has made a critical contribution to knowledge through the finding that to altogether decrease corruption in project planning and execution, attention should be focused on the logic and performance of anti-corruption systems. The anti-corruption systems to focus on are contractual compliance, financial accountability, KPIs, international and national standards, oversight by NGOs, and increased information access. Also, this study has made known the need to create a framework within which the planned effect of anti-corruption measures can be seen before implementation. This pre-implementation profiling ought to reveal the logic of the anti-corruption measures. The study has provided a mechanism for making anti-corruption programmes methodical. By choosing anti-corruption systems as indicated by their logic and viability, an anti-corruption programme could be planned to save an individual in an inert and innately corrupt climate and save the general public and organisations from corrupt individuals. The study revealed that no single methodology can be utilised to battle corruption in the construction sector owing to its complex nature and sophisticated corruption. The sector requires anti-corruption systems that can induce exclusive standards of conduct and ethics in the sector, as well as meet the international demand for battling corruption and further developing accountability, probity, and transparency in governance.

Implications, limitations, and future studies

The anti-corruption systems that would significantly impact corruption in the construction sector include contractor blacklisting and de-registration, oversight by NGOs, increased information access, and KPIs. Others are technical auditing, financial accountability, contractual compliance, adherence to international and national standards, project governance, cashless policies, due process, social accountability, political accountability, and contract monitoring. Due to their logic, these anti-corruption systems would induce exclusive standards of conduct and ethics in the sector. They would also ensure an effective anti-corruption campaign in the short and long term and address the genuine essentials of corruption because they represent various classifications of anti-corruption systems. Adoption of integrated anti-corruption systems would account for variations in anti-corruption system effectiveness and political interference caused by administration conditions, poor leadership, regulatory setbacks, and the working environment. It will also protect anti-corruption programmes from relying on legal and financial establishments or from being hampered due to shortcomings and internal corruption in legal and financial institutions. Likewise, explicit anti-corruption systems should be considered for limiting corruption at individual, project, organisational, governmental, and national levels.

This study is restricted by not considering the public office holders that partake in project planning and execution in various departments and ministries as research participants. Future studies would profit from their bits of insight. Such studies would extend the generalizability of this study’s findings. Although the adoption of random sampling techniques for this research has made it generalizable to similar circumstances, the study findings and concepts of anti-corruption systems’ logic are applicable globally for designing anti-corruption systems and could serve as a theoretical framework for future studies. Using the concepts of anti-corruption systems’ logic will not only enhance the external validity of the study and support the replication of this study in similar settings, but also improve the criteria, standards, and level of rigour of similar research. The effect of public tendering procedures and selection criteria on the construction sector’s corruption dynamics should be explored in future studies. The forms, structure, and moral contents of the politics of collusive tendering in the Nigerian construction sector should also be explored.

References

Adekunle, A., Adewale, A.K., Olaifa, O.A. and Ukoh, S.N.B., 2019. Statistical Study on Types, Causes, Effects and Remedies of Corrupt Practices in Construction Industries in Nigeria. International Journal of Advances in Scientific Research and Engineering, 5(9), pp.71-80. https://doi.org/10.31695/IJASRE.2019.33493

Adnan, H., Hashim, N., Mohd, N. and Ahmad, N., 2012. Ethical issues in the construction industry: Contractor’s perspective. Procedia-social and behavioural sciences, 35, pp.719-27. https://doi.org/10.1016/j.sbspro.2012.02.142

Aduwo, E.B., Ibem, E.O., Afolabi, A.O., Oluwnmi, A.O., Tunji-Olayeni, P.F., Ayo-Vaughan, E.A. and Oni, A.A., 2020. Exploring anti-corruption capabilities of e-procurement in construction project delivery in Nigeria. Construction Economics and Building, 20(1), pp.56-76. https://doi.org/10.5130/AJCEB.v20i1.6964

Afolabi, A., Ibem, E., Aduwo, E. and Tunji-Olayeni, P., 2020. Digitizing the grey areas in the Nigerian public procurement system using e-Procurement technologies. International Journal of Construction Management, pp.1-10. https://doi.org/10.1080/15623599.2020.1774836

Al-Hojjaj, A.P.Y.A., 2020. The national system of integrity: a novel approach to preventing corruption and enhancing administrative health. PalArch’s Journal of Archaeology of Egypt/Egyptology, 17(6), pp.16164-78.

Badawi, A. and AlQudah, A., 2019. The impact of anti-corruption policies on the profitability and growth of firms listed in the stock market: Application on Singapore with a panel data analysis. The Journal of Developing Areas, 53(1), pp.179-204. https://doi.org/10.1353/jda.2019.0011

Bashir, Y.M., 2016. Effects of treasury single account on public finance management in Nigeria. Research Journal of Finance and Accounting, 7(6), pp.164-70.

Bertot, J.C., Jaeger, P.T. and Grimes, J.M., 2010. Using ICTs to create a culture of transparency: E-government and social media as openness and anti-corruption tools for societies. Government information quarterly, 27(3), pp.264-71. https://doi.org/10.1016/j.giq.2010.03.001

Cartwright, S., Liu, H. and Raddats, C., 2021. Strategic use of social media within business-to-business (B2B) marketing: A systematic literature review. Industrial Marketing Management, 97, pp.35-58. https://doi.org/10.1016/j.indmarman.2021.06.005

Dza, M., Kyeremeh, E., Dzandu, S.S. and Afran, S., 2018. Corruption in Public Procurement in Ghana: societal norm or deviant behaviour? Archives of Business Research, 6(12). https://doi.org/10.14738/abr.612.5719

Ebekozien, A., 2020. Corrupt acts in the Nigerian construction industry: is the ruling party fighting corruption? Journal of Contemporary African Studies, 38(3), pp.348-65. https://doi.org/10.1080/02589001.2020.1758304

Erol, I. and Unal, U., 2015. Role of Construction Sector in Economic Growth: New Evidence from Turkey (No.68263). University Library of Munich, Germany.

Etikan, I. and Bala, K., 2017. Sampling and sampling methods. Biometrics and Biostatistics International Journal, 5(6), pp.00149. https://doi.org/10.15406/bbij.2017.05.00149

Evans, R.H., 1996. An analysis of criterion variable reliability in conjoint analysis. Perceptual and motor skills, 82(3), pp.988-90. https://doi.org/10.2466/pms.1996.82.3.988

Fan, D., Yeung, A.C., Yiu, D.W. and Lo, C.K., 2022. Safety regulation enforcement and production safety: The role of penalties and voluntary safety management systems. International Journal of Production Economics, 248, pp.108481. https://doi.org/10.1016/j.ijpe.2022.108481

Folorunso, O.O. and Simeon, A.O., 2021. The gains and the pains of integrated payroll and personnel information systems (IPPIS) policy implementation in Nigeria. Journal of Human Resource and Sustainability Studies, 9(4), pp.551-69. https://doi.org/10.4236/jhrss.2021.94035

Hamilton-Hart, N., 2001. Anti-corruption strategies in Indonesia. Bulletin of Indonesian Economic Studies, 37(1), pp.65-82. https://doi.org/10.1080/000749101300046519

Hetami, A.A. and Aransyah, M.F., 2020. Investigation of corruption prevention plan in construction industries. Jurnal Perspektif Pembiayaan dan Pembangunan Daerah, 8(1), pp.51-64. https://doi.org/10.22437/ppd.v8i1.8722

Inuwa, I., Ononiwu, C. and Kah, M.M., 2020. Dimensions that characterize and mechanisms that cause the misuse of information systems for corrupt practices in the Nigerian public sector. The Electronic Journal of Information Systems in Developing Countries, 86(6), pp.12136. https://doi.org/10.1002/isd2.12136

Inuwa, I., Ononiwu, C., Kah, M.M. and Quaye, A.K., 2019. Mechanisms fostering the misuse of information systems for corrupt practices in the Nigerian public sector. In: Petter Nielsen and H.C. Kimaro eds. Information and Communication Technologies for Development. Proceedings of the International Conference on Social Implications of Computers in Developing Countries, Dar es Salaam, Tanzania, 1-3 May 2019, pp.122-34. Cham, Switzerland: Springer. https://doi.org/10.1007/978-3-030-19115-3_11

Jang, H.S., Park, H.K. and Lee, Y.S., 2012. A study on strategies for enhancing the transparency of the domestic construction industry through foreign cases. KSCE Journal of Civil and Environmental Engineering Research, 32(3D), pp.231-37.

Joseph, C., Gunawan, J., Sawani, Y., Rahmat, M., Noyem, J.A. and Darus, F., 2016. A comparative study of anti-corruption practice disclosure among Malaysian and Indonesian Corporate Social Responsibility (CSR) best-practice companies. Journal of cleaner production, 112, pp.2896-2906. https://doi.org/10.1016/j.jclepro.2015.10.091

Krastev, I., 2003. Corruption, anti-corruption sentiments, and the rule of law. In: Andrea Krizan and Violetta Zentai, eds. Reshaping Globalization: Multilateral Dialogues and New Policy Initiatives. Ch.II, pp.135-54.

Kuoribo, E., Owusu-Manu, D.G., Yomoah, R., Debrah, C., Acheampong, A. and Edwards, D.J., 2021. Ethical and unethical behaviour of built environment professionals in the Ghanaian construction industry. Journal of Engineering, Design and Technology, [e-journal] 21(3), pp.840-61. https://doi.org/10.1108/JEDT-02-2021-0108

Ledeneva, A.V. and Shekshnia, S., 2011. Doing business in Russia: informal practices and anti-corruption strategies. Russie. Nei. Visions, (58). Paris, France: IFRI.

Lehtinen, J., Locatelli, G., Sainati, T., Artto, K. and Evans, B., 2022. The grand challenge: Effective anti-corruption measures in projects. International Journal of Project Management, 40(4), pp.347-61. https://doi.org/10.1016/j.ijproman.2022.04.003

Mackey, T.K. and Cuomo, R.E., 2020. An interdisciplinary review of digital technologies to facilitate anti-corruption, transparency and accountability in medicines procurement. Global health action, 13(sup1), pp.1695241. https://doi.org/10.1080/16549716.2019.1695241

Maruichi, D. and Abe, M., 2019. Corruption and the business environment in Vietnam: Implications from an empirical study. Asia and the Pacific Policy Studies, 6(2), pp.222-45. https://doi.org/10.1002/app5.275

Mattoni, A. and Odilla, F., 2021. Digital Media, Activism, and Social Movements’ Outcomes in the Policy Arena. The Case of Two Anti-Corruption Mobilizations in Brazil. Partecipazione e conflitto, 14(3), pp.1127-50.

Maxwell, S.E., 2000. Sample size and multiple regression analysis. Psychological methods, 5(4), pp.434. https://doi.org/10.1037/1082-989X.5.4.434

McCusker, R., 2006. Review of anti-corruption strategies (pp.4-5). Canberra: Australian Institute of Criminology.

Mikail, I.K., 2018. Strategies for combating corruption in Nigeria 1999-2015: effectiveness and challenges. PhD. Universiti Utara Malaysia.

Mikail, I.K., Abbas, S.S., Bint Ismail, N. and Abdullah, M.A.I.L.I., 2017. Comparative studies on strategies for combating corruption between Nigeria and Iraq. Journal of Governance and Development, 13(2), pp.15-33.

Nelson, K.L. and Afonso, W.B., 2019. Ethics by design: The impact of the form of government on municipal corruption. Public Administration Review, 79(4), pp.591-600. https://doi.org/10.1111/puar.13050

Nnadozie, B.C., 2021. Public Perceptions of Nigeria Police Monetary Bribery in Awka, Nigeria. PhD. Walden University.

Oberoi, R., 2014. Mapping the matrix of corruption: Tracking the empirical evidences and tailoring responses. Journal of Asian and African Studies, 49(2), pp.187-214. https://doi.org/10.1177/0021909613479319

Oladinrin, T.O., Ogunsemi, D.R. and Aje, I.O., 2012. Role of construction sector in economic growth: Empirical evidence from Nigeria. FUTY Journal of the Environment, 7(1), pp.50-60. https://doi.org/10.4314/fje.v7i1.4

Olugboyega, O., Oyeyemi, O.A., Ehis, O.G. and Aigbavboa, C., 2023. Effects of Building contractors’ Value Systems on Corruption Manifestations in Nigeria’s Construction Sector. International Journal of Construction Education and Research, [e-journal] pp.1-21. https://doi.org/10.1080/15578771.2023.2203956

Omadjohwoefe, S., 2014. Corruption and sustainable development in Nigeria: The imperative of a trado-religious anti-corruption strategy. International Journal of Business and Social Science, 5(1), pp.223-30.

Owusu, E.K., Chan, A.P., DeGraft, O.M., Ameyaw, E.E. and Robert, O.K., 2019. A contemporary review of anti-corruption measures in construction project management. Project Management Journal, 50(1), pp.40-56. https://doi.org/10.1177/8756972818808983

Paterson, A.S., Changwony, F. and Miller, P.B., 2019. Accounting control, governance and anti-corruption initiatives in public sector organisations. The British Accounting Review, 51(5), pp.100844. https://doi.org/10.1016/j.bar.2019.100844

Peisakhin, L. and Pinto, P., 2010. Is transparency an effective anti‐corruption strategy? Evidence from a field experiment in India. Regulation and Governance, 4(3), pp.261-80. https://doi.org/10.1111/j.1748-5991.2010.01081.x

Quah, J.S.T., 2013. Different Paths to Curbing Corruption: Lessons from Denmark, Finland, Hong Kong, New Zealand and Singapore. In: Research In Public Policy Analysis And Management Vol 23. Leeds, England: Emerald Publishing. https://doi.org/10.1108/S0732-1317(2013)0000023012

Rizk, R., Sobh, D. and Hamzeh, F., 2018. Studying the mindset of corruption in the construction industry-a lean perspective. 26th Annual Conference of the International Group for Lean Construction (IGLC), 18-22 July 2018, Chennai, India. https://doi.org/10.24928/2018/0282

Sheryazdanova, G. and Butterfield, J., 2017. E-government as an anti-corruption strategy in Kazakhstan. Journal of Information Technology and Politics, 14(1), pp.83-94. https://doi.org/10.1080/19331681.2016.1275998

Sibanda, O., 2005. The South African corruption law and bribery of foreign public officials in international business transactions: a comparative analysis. South African Journal of Criminal Justice, 18(1), pp.1-23.

Sichombo, B., Muya, M., Shakantu, W. and Kaliba, C., 2009. The need for technical auditing in the Zambian construction industry. International Journal of Project Management, 27(8), pp.821-32. https://doi.org/10.1016/j.ijproman.2009.02.001

Taber, K.S., 2018. The use of Cronbach’s alpha when developing and reporting research instruments in science education. Research in science education, 48(1), pp.1273-96. https://doi.org/10.1007/s11165-016-9602-2

Tacconi, L. and Williams, D.A., 2020. Corruption and anti-corruption in environmental and resource management. Annual Review of Environment and Resources, 45, pp.305-29. https://doi.org/10.1146/annurev-environ-012320-083949

Turner, P., 2020. Critical values for the Durbin-Watson test in large samples. Applied Economics Letters, 27(18), pp.1495-99. https://doi.org/10.1080/13504851.2019.1691711

Ulain, N. and Hussain, F., 2020. Fighting governmental corruption in Pakistan: An evaluation of anti-corruption strategies. Hrvatska i komparativna javna uprava: časopis za teoriju i praksu javne uprave, 20(3), pp.439-68. https://doi.org/10.31297/hkju.20.3.2

VanVoorhis, C.W. and Morgan, B.L., 2007. Understanding power and rules of thumb for determining sample sizes. Tutorials in quantitative methods for psychology, 3(2), pp.43-50. https://doi.org/10.20982/tqmp.03.2.p043

Vian, T., 2020. Anti-corruption, transparency and accountability in health: concepts, frameworks, and approaches. Global health action, 13(sup1), 1694744. https://doi.org/10.1080/16549716.2019.1694744

Zou, P.X., 2006. Strategies for minimizing corruption in the construction industry in China. Journal of construction in Developing Countries, 11(2), pp.15-29.